_edited.png)

Family Income Policies: Secure Your Family’s Financial Future

- dustinjohnson5

- Oct 16, 2025

- 15 min read

A family income policy isn't your typical life insurance. Instead of paying out a huge, one-time check, it delivers a steady, predictable monthly income to your family. It's designed to step in and replace your paycheck, ensuring your loved ones can keep up with the mortgage, bills, and everyday costs without financial disruption.

Think of it as a financial safety net woven to match the rhythm of your family's life.

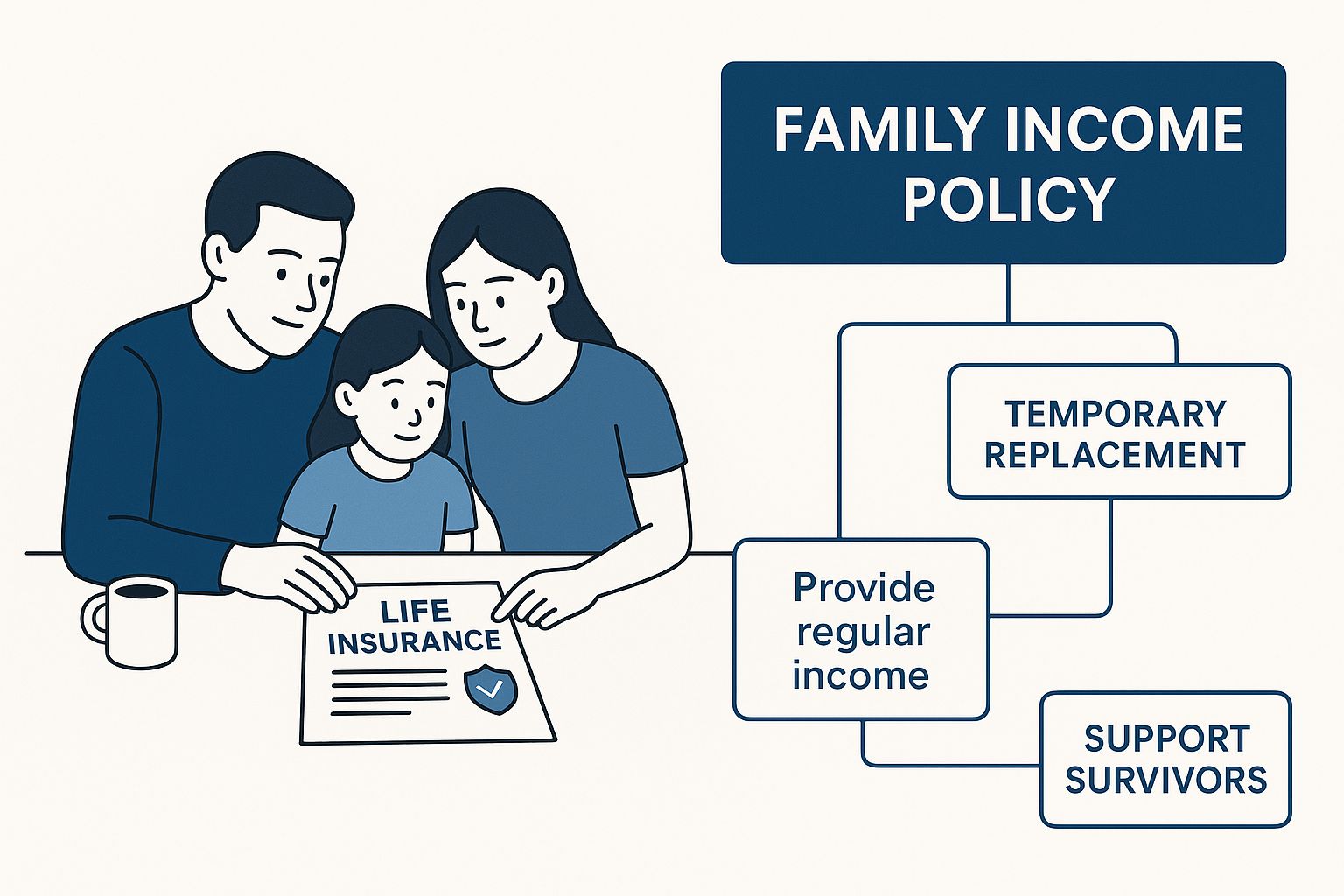

What Are Family Income Policies

Every month, your household runs on a predictable cycle of income and expenses. The mortgage is due, the car payment comes out, and you have to buy groceries. A family income policy is built around that very same rhythm.

Instead of dropping a massive lump sum into your family's lap while they're grieving—a sum they'd then have to figure out how to manage—this policy provides a consistent, familiar income stream. It removes the enormous pressure of having to invest a large amount of money wisely during an already overwhelming time. It's the difference between winning the lottery and simply having a lost salary replaced.

The infographic below helps paint a clearer picture of how this kind of policy fits right into a family's financial plan.

As you can see, it's a tool designed for stability, making sure the day-to-day financial obligations are met, no matter what.

How The Payout Structure Works

The mechanics are refreshingly simple. First, you choose a policy term—say, 20 or 30 years—and decide on a monthly income amount your family would need to live comfortably. If you pass away at any point during that term, the policy kicks in and starts sending that monthly payment to your beneficiaries.

But here’s the key part: the payments only last for the remainder of the original policy term.

Let's break that down. If you have a 30-year policy and die five years in, your family gets monthly checks for the remaining 25 years. If you pass away 29 years into the term, they receive payments for just one year. This structure, often known as Family Income Benefit insurance, is specifically designed to cover the years when your family is most financially vulnerable, like when the kids are still at home.

The core benefit is predictability. A family income policy offers a structured payout that aligns with a household's regular budget, removing the guesswork and investment risk associated with a lump-sum payment during a time of emotional distress.

This "decreasing liability"—the total potential payout gets smaller as you near the end of the term—is exactly why these policies are often more affordable than a standard term life policy for the same initial coverage amount.

Family Income Policy vs Lump-Sum Term Life Insurance

It's crucial to understand the difference between a steady income stream and a single, large payout. They both offer vital financial protection, but they solve different problems.

A lump-sum benefit is fantastic for wiping out big, immediate expenses. Think paying off the mortgage in one go or funding a college education fund. A family income policy, on the other hand, excels at replacing that lost monthly salary for all the ongoing costs of living.

Here’s a quick table to make the comparison crystal clear.

Feature | Family Income Policy | Lump-Sum Term Life Insurance |

|---|---|---|

Payout Structure | A series of regular monthly payments for the remaining policy term. | A single, tax-free payment made to beneficiaries upon death. |

Primary Purpose | To replace lost monthly income and cover ongoing living expenses. | To cover large, immediate debts or provide a substantial inheritance. |

Financial Management | Simplified for beneficiaries; no complex investment decisions needed. | Beneficiaries must manage and invest the large sum to make it last. |

Affordability | Often more cost-effective due to the decreasing total payout over time. | Premiums are based on a fixed death benefit for the entire term. |

Ultimately, there’s no single "best" option. The right choice really comes down to your family's specific financial situation and how comfortable your beneficiaries would be managing a large sum of money on their own.

Why a Monthly Payout Creates Real Peace of Mind

The biggest advantage of a family income policy goes way beyond the numbers on a spreadsheet; it taps right into human psychology. When a tragedy strikes, the last thing a grieving family needs is to suddenly become high-stakes financial managers. Imagine receiving a massive, life-altering check—it can feel less like a lifeline and more like an overwhelming burden, forcing you to make huge investment decisions under intense emotional stress.

A steady, monthly payout completely removes that pressure. It turns the abstract idea of a death benefit into something real and tangible: everyday security. There's no complex portfolio to manage or stock market to worry about. Instead, there's just the quiet confidence that the mortgage will be paid, the groceries will be bought, and the lights will stay on next month.

What this structure really provides is the single most valuable thing in a crisis: breathing room. It gives a family the space to grieve and adjust without the immediate, terrifying fear of financial ruin. The focus shifts from, "How on earth will we manage this huge sum of money?" to "We are going to be okay this month, and the next, and the next."

Maintaining a Sense of Normalcy

Think about a family like the Millers. Mark was a skilled tradesman and the main breadwinner, while Sarah ran their busy household with two young kids. They were comfortable but lived on a careful budget built around Mark's reliable income.

When Mark died suddenly, Sarah’s world fell apart. If she’d received a big lump-sum payout, she would have been paralyzed with questions. Pay off the mortgage? Invest? Put it all in savings? Every option would have felt monumental and terrifying.

Instead, their family income policy kicked in. A predictable check arrived every month, replacing almost exactly what Mark used to bring home. In a sea of uncertainty, that consistency was a powerful emotional anchor.

For a family navigating loss, financial predictability is a form of emotional stability. A monthly income stream allows them to maintain routines and make clear-headed decisions, preserving a sense of normalcy when everything else feels chaotic.

This regular income meant Sarah didn’t have to make any drastic decisions right away. The kids stayed in their school, kept up with their activities, and remained in the only home they’d ever known. The rhythm of their daily life, though forever altered, had a financial foundation that didn’t crumble.

The Power of Budgeting and Stability

The monthly payout model let Sarah keep managing the household finances just like she always had. She already knew how to budget with a monthly income—it was a skill she'd used for years.

This simple, familiar structure empowered her to:

Cover essential bills without stress. The mortgage, utilities, and car payments were handled as usual, keeping the threat of debt at bay. For many families, just keeping the lights on can take up over 4.4% of their annual income, so this stability is absolutely critical.

Plan for childcare costs. Sarah could afford reliable childcare, which gave her the time she needed to handle personal affairs and eventually think about re-entering the workforce on her own terms, not out of desperation.

Avoid lifestyle disruption. The family could carry on without the immediate shock of having to downsize their home or drastically cut back on everyday needs.

This stability prevents a personal tragedy from becoming an instant financial catastrophe. We see this in public economic security programs, where predictable support helps families build a path toward long-term independence. A family income policy acts as a private, immediate version of that same support system.

Ultimately, the real peace of mind comes from getting rid of the "what ifs." What if the market crashes? What if I make a bad investment? What if the money runs out too soon? A family income policy replaces all those anxieties with the simple, powerful assurance that next month's needs will be met.

What Determines Your Policy Eligibility and Cost

When you apply for a family income policy, the insurance company is really just trying to answer one big question: How likely are we to have to pay out a claim on this policy? The answer they come up with determines if you're approved and exactly how much you'll pay. It’s all a game of risk assessment, where they look at a bunch of personal factors to get a clear picture of your life expectancy.

Think of it like putting together a puzzle. The insurer gathers different pieces of information about you to see how they all fit. Each piece helps them understand the level of risk they’re taking on by insuring you. Let's break down the most important pieces of that puzzle.

Core Factors Insurers Evaluate

Your application will dig into a few key areas of your life. Don't worry, they aren't just being nosy. They're using decades of statistical data to make an educated guess about your long-term health.

Here are the main things they'll be looking at:

Your Age: This one is pretty simple. Statistically speaking, the younger you are when you get life insurance, the less likely you are to pass away during the policy's term. That’s why younger applicants almost always get the lowest rates.

Your Health History: You can expect a detailed medical questionnaire and, most of the time, a simple medical exam. Insurers look at your current health, your family's medical history (especially for things like heart disease or cancer), your height-to-weight ratio, cholesterol, and blood pressure.

Lifestyle Choices: How you live your life day-to-day really matters. Are you a smoker? This is a huge red flag for insurers and can jack up your premium by 50% or even more. They'll also ask about your alcohol consumption and any history of substance abuse.

Your Occupation and Hobbies: A desk job is seen as much less risky than being a pilot, a commercial diver, or a roofer. The same goes for hobbies. If you spend your weekends skydiving or rock climbing, your premiums will reflect that higher risk.

The whole point of this underwriting process is to put you into a specific risk class. These range from "Preferred Plus" for the healthiest folks down to "Standard" or even "Substandard" ratings for people with health issues. Where you land directly determines your final premium.

How These Factors Impact Your Premiums

To see how this plays out in the real world, let's look at two different people applying for the same $5,000 per month, 20-year family income policy.

Scenario 1: The Low-Risk Applicant

Applicant: A 30-year-old woman, non-smoker.

Health: She's in great health, has no chronic conditions, and a clean family medical history.

Occupation: Works as an office manager.

Result: She's the ideal candidate. She'll almost certainly qualify for a "Preferred Plus" rating and get a very low monthly premium because her age and healthy lifestyle present almost no risk to the insurer.

Scenario 2: The Higher-Risk Applicant

Applicant: A 45-year-old man who smokes.

Health: His blood pressure is a bit high, and there's a history of heart problems in his family.

Occupation: Long-haul truck driver.

Result: His age, smoking habit, and health profile put him in a much higher risk category. For the exact same coverage, his premium could easily be four to five times higher than the first applicant's. It’s a perfect example of how risk translates directly into cost.

Of course, the amount of income you want to replace is a major factor in the cost, too. A policy that provides a bigger monthly benefit will naturally have a higher premium. With the median household income in the U.S. recently sitting around $83,730, you can see how significant the financial gap a policy might need to fill can be. You can dig into more about income statistics and what they mean for families by checking out the latest Census Bureau data.

How Family Economic Security Looks Around the World

A family income policy is a personal financial decision, but it doesn't exist in a vacuum. The real value of a policy like this is tied directly to the country you live in and the economic safety nets—or lack thereof—that are already in place.

Across the globe, nations have wildly different approaches to family financial stability. Some have robust, government-led social programs, while others rely almost entirely on private insurance as the main line of defense. Understanding this bigger picture helps you see exactly where a family income policy fits into your own financial puzzle.

A Nation's Wealth Shapes Its Safety Net

The best way to get a handle on this is to look at how the World Bank classifies countries by income. This isn't just an economic exercise; it shows how a country's wealth directly impacts the kind of support its families can expect.

The World Bank sorts countries into four groups based on their Gross National Income (GNI) per person. The latest 2025 update includes 93 high-income countries, 55 upper-middle-income, 50 lower-middle-income, and 25 low-income nations. This matters because it influences what each government can prioritize—from comprehensive social welfare in richer countries to basic needs like food security in developing ones. You can see a great breakdown of these global income level classifications by country.

This economic reality is what determines the mix of public versus private solutions for protecting a family’s future.

High-Income Countries: Layering On Protection

In high-income nations like the United States, Canada, and most of Western Europe, governments typically provide a solid foundation of social safety nets. Think of things like:

Social Security Survivor Benefits: Payments from the government that go to the surviving spouse and kids of a worker who has passed away.

National Health Services: Public healthcare that prevents medical debt from piling up on top of a family tragedy.

Unemployment and Disability Insurance: Programs that provide an income stream if the main breadwinner loses their job or can't work anymore.

In places like these, a family income policy acts as a crucial supplementary layer of financial security. Government benefits provide a floor, but they almost never replace a full professional’s salary. This is where the policy steps in to fill the gap, making sure a family can keep up with their mortgage, maintain their standard of living, and still save for big goals like college.

In wealthier nations, a family income policy isn’t just about survival. It's about protecting a family's lifestyle, legacy, and long-term dreams when state support alone isn’t enough.

Lower-Income Countries: A Foundational Lifeline

It's a completely different story in lower- and middle-income countries, where government safety nets are often thin or simply don't exist. Families might have very little public support to rely on if the primary earner dies. Here, economic security is about the basics—putting food on the table, not preserving a certain lifestyle.

In this context, a private family income policy shifts from being a helpful supplement to a foundational pillar of survival. It can be the one and only thing standing between a family and poverty, ensuring they can afford housing, food, and an education for their children.

For these families, the steady, predictable income from a policy isn't a comfort; it's a lifeline. It provides a stability the government can't offer, giving the next generation a chance to move forward even after a devastating loss. It just goes to show how the same insurance product can have a profoundly different—and equally vital—impact depending on the world around it.

How to Choose the Right Family Income Policy

Picking a family income policy is more than just a financial transaction—it’s about building a safety net that fits your family perfectly. You're not just buying a policy; you're designing a financial bridge that can carry your loved ones forward if you're not there. The goal is to replace your income so seamlessly that their lives can continue with stability and security.

This isn't a time for guesswork. It's about taking a clear, honest look at your family's finances to land on a monthly income stream that’s just right.

Calculate Your Family's True Monthly Need

First things first: you need to nail down the exact monthly income your family would need to maintain their lifestyle. It’s tempting to just use your take-home pay as a benchmark, but you have to dig deeper. A truly accurate number comes from a detailed budget of every single expense you cover.

To get to that number, make sure you account for everything:

Housing Costs: This is the big one—your mortgage or rent payment, plus property taxes and homeowners insurance.

Daily Living Expenses: Think about groceries, utilities, transportation (car payments, gas, insurance), and phone and internet bills.

Child-Related Costs: This category is crucial. Include childcare, school tuition, sports, music lessons, and, of course, contributions to college savings.

Debt Payments: List out any outstanding student loans, credit card balances, car loans, or personal loans.

Healthcare and Insurance: Don't forget health insurance premiums, co-pays, and any other regular medical costs.

Add it all up. Then, subtract any income your spouse or partner would continue to earn. What's left is your target monthly benefit. That’s the magic number your policy needs to deliver each month to keep your family whole.

Determine the Right Policy Term

Next up, you need to decide how long this income stream should last. The term of your family income policy should line up with your most significant financial obligations. Think of it as a countdown clock, set to the end of your family's most financially vulnerable period.

A great way to do this is to tie the term to a major life milestone. For instance:

Until your youngest child is independent: If your youngest is three years old, a 20-year or 25-year term would see them through high school and college.

Until the mortgage is paid off: Have 18 years left on your home loan? A 20-year term makes sure that roof stays over their heads, free and clear.

The ideal term length isn't just a random number. It should directly map to the period when the loss of your income would hit your family the hardest.

This targeted approach is what makes these policies so smart and cost-effective. You're only paying for coverage during the years it's absolutely critical, which helps keep the premiums down. Setting yourself up for success like this is the foundation of smart financial planning, and it all starts when you understand how to set financial goals that actually work.

Compare Quotes and Read the Fine Print

Once you know your ideal monthly benefit and term length, it’s time to shop around. Don’t ever take the first quote you see. Insurers all have their own ways of calculating risk, meaning you can find wildly different prices for the exact same coverage.

But as you compare, look past the price tag. The devil is in the details, so you need to read the policy documents carefully. Here’s what to look for:

Conversion Options: Does the policy let you convert it to a permanent life insurance plan down the road without another medical exam? This is a huge benefit, offering flexibility if your life circumstances change.

Riders and Add-Ons: See what riders are available. A waiver of premium rider, for example, would cover your premiums if you became disabled and couldn't work. It’s a valuable backup plan.

Exclusions: Get crystal clear on what the policy doesn’t cover. Most policies have a two-year "contestability period" where the insurer can investigate and deny a claim if you left out important information on your application.

Finally, don't be afraid to talk to a qualified, independent financial advisor. A professional can help you cut through the jargon, compare policies objectively, and make sure the plan you choose is genuinely the best fit for your family’s future.

Common Questions About Family Income Policies

It's completely normal to have a few questions when you're looking at a specific financial tool like a family income policy. Even after you’ve got the basics down, a few details might still feel a bit fuzzy.

Let's walk through some of the most common questions people ask. We'll tackle them one by one to give you the clarity you need to make a confident decision.

What Happens If I Outlive the Policy?

This is probably the most common question out there, and the answer is straightforward. If you outlive the policy term, the policy simply ends. It expires, you stop paying the premiums, and that's it—no payout is made.

The best way to think about it is like your home or auto insurance. You pay for it to protect against a "what if" scenario. The premiums you paid bought you years of invaluable peace of mind, knowing your family was protected during a time they would have needed it most.

Can I Have More Than One Life Insurance Policy?

Absolutely. In fact, it's a very common strategy for people to "stack" different policies to meet different needs. For example, you might have a family income policy to replace your paycheck for day-to-day living expenses and a separate, smaller lump-sum term policy designated to pay off the mortgage.

This approach lets you build a truly customized financial safety net. You can earmark specific policies for specific goals, making sure everything is covered without overpaying for coverage you don't actually need.

Are the Monthly Payouts Taxable?

For most people in the United States, the answer is a resounding no. Life insurance death benefits, whether they arrive as a single check or a stream of monthly payments, are generally not subject to federal income tax. This is a huge advantage, as it means every dollar of the benefit goes directly to your beneficiaries.

That said, estate tax laws can get tricky and vary from state to state. It's always a smart move to chat with a financial advisor or tax professional to see how this applies to your specific situation.

The tax-free nature of the benefit is a powerful feature of family income policies. It ensures the income your family receives is the income they can actually spend on their needs, without a portion being lost to taxes.

Can I Change My Policy After I Buy It?

This really depends on the fine print of your specific policy. Generally, you can't just call up and increase the monthly benefit without a new application and medical review. However, many policies do come with built-in flexibility.

The key feature to look for is a conversion option. This lets you convert your term policy into a permanent one (like whole life) down the road, without having to pass another medical exam. This can be a lifesaver if your financial situation changes or you develop a health condition later in life.

Global economic shifts also underscore the need for financial security. For instance, in June 2025, the World Bank adjusted the International Poverty Line from $2.15 to $3.00 per day. This single change instantly reclassified about 125 million people as living in extreme poverty, showing just how quickly the definition of financial need can change. It’s a powerful reminder of why having a reliable financial plan is so important. You can find more details about this new international poverty line on Our World in Data.

What If My Family Would Rather Have a Lump Sum?

This is a great question and an important feature to ask about. Many family income policies offer what's called a "commutation" rider or option. This gives your beneficiary the choice to take the present value of all the future monthly payments as one single, lump-sum payout instead.

Having this option built-in provides incredible flexibility. While a steady monthly income is great for stability, there might be a situation where a large, upfront sum makes more sense for your family at that time. It really offers the best of both worlds.

At America First Financial, we believe in providing clear, straightforward solutions that protect what matters most—your family. Our policies are designed to offer robust financial security without the noise of political agendas. If you're ready to build a reliable safety net for your loved ones, you can get a free, no-hassle quote in just a few minutes.

Secure your family's future today by exploring your options at https://www.americafirstfinancial.org.

Comments