_edited.png)

Smart Generational Wealth Planning That Actually Works

- dustinjohnson5

- Jun 10, 2025

- 14 min read

The Wealth Transfer Revolution Happening Right Now

Something massive is brewing in the world of family wealth, and frankly, most folks haven't even noticed. I've spent years chatting with wealth advisors, and they're all seeing the same pattern – the old playbook just isn't cutting it anymore. We're smack-dab in the middle of a historic wealth transfer, but the traditional methods are falling flat. Generational wealth planning needs a fresh perspective. Why? Because simply holding onto wealth isn't enough; families who are really thinking ahead are focused on making it grow.

This isn't about some get-rich-quick scheme. It's about building a legacy that lasts. It's about understanding that the financial choices we make today have a ripple effect for generations to come. Think of it like planting a tree. You don't just plop it in the dirt and forget about it. You nurture it, you prune it, and you make sure it has everything it needs to flourish, not just while you're around, but for the generations that follow.

One of the biggest trends in this area is the huge transfer of wealth we're expecting to see, mostly in the United States. Baby Boomers are projected to pass down something like $6 trillion, while Gen X is poised to inherit a whopping $39 trillion. This massive influx of capital presents both incredible opportunities and some serious challenges. Want to learn more about this wealth transfer? Check out this article: Great Wealth Transfer Impact. The big question is: how are families going to navigate this transition?

Navigating the Shifting Sands of Wealth

The old-school strategies focused mainly on preservation—minimize taxes, set up trusts, and cross your fingers the next generation figures it out. But things have changed. Inflation is eating away at purchasing power, markets are all over the place, and let's be honest, younger generations have different values and priorities. Handing over a trust fund just doesn't cut it anymore. True generational wealth means preparing the next generation to not just receive wealth, but to actually manage it, grow it, and use it wisely.

Think about a family business passed down over the years. The first generation builds it brick by brick, the second generation expands it, but what happens to the third? Without the same entrepreneurial spirit and financial know-how, things can fall apart. Wealth is no different. It takes active management and a shared family vision to really thrive. That's where the real revolution lies - in understanding that true generational wealth isn't just about the dollars and cents, it's about preparing future generations to be responsible stewards of that wealth.

Let's take a look at the projected wealth transfer over the next couple of decades. The table below illustrates the key challenges each generation faces.

Generational Wealth Transfer Timeline Breakdown of expected wealth transfers by generation over the next two decades

Generation | Expected Transfer Amount | Timeline | Key Challenges |

|---|---|---|---|

Baby Boomers | ~$6 Trillion | Current - 2040 | Managing healthcare costs, ensuring retirement income, effectively transferring assets |

Gen X | ~$39 Trillion | 2030 - 2050 | Balancing care for aging parents and their own children, navigating volatile markets, preparing for a longer lifespan |

Millennials | N/A (Will inherit from Gen X) | 2050+ | Dealing with potentially higher debt levels, adapting to rapidly changing technology, fostering a sense of financial responsibility |

This table highlights the unique circumstances each generation faces in this massive wealth transfer. Understanding these challenges is the first step in developing a robust and effective generational wealth plan.

Building Your Foundation Before Getting Fancy

Most wealth planning advice drives me crazy. Everyone jumps into the complicated stuff before nailing down the basics. I’ve seen families get so tangled up in trust structures that they forgot to shore up their core finances. So, let's talk about the fundamentals. The families I've known who've built lasting wealth? They all started with a rock-solid foundation. This means rethinking everything from your emergency fund to insurance and how you handle debt.

Wealthy families still need emergency funds. But the purpose is different. It's not about covering a broken-down car; it's about having the liquidity to jump on opportunities or weather unexpected storms. And you do this without touching your long-term investments. Think of it as a financial shock absorber for your generational wealth plan. One family I work with keeps a large cash reserve specifically to buy up investments when the market dips. They’re able to invest when others are panicking, which accelerates their long-term growth.

Insurance also plays a key role. But it’s about strategic protection, not over-insuring. Focus on catastrophic events that could derail generational wealth—disability, liability lawsuits, and key-person insurance if you own a business. Don't sweat the small stuff you can easily cover yourself. I’ve watched families pour thousands into unnecessary premiums, money that could have earned far better returns invested for the long haul. It’s all about balancing protection with smart resource allocation. The United States remains the leading global hub for private wealth – a critical factor in generational wealth planning on a global scale. In 2025, the U.S. was home to over six million high-net-worth individuals (HNWIs) with at least $1 million in investable assets. You can discover more insights on this wealth concentration here.

Smart Debt and Cash Flow Management

Successful families understand that debt isn’t always bad. Used strategically, low-interest debt can leverage investments and accelerate wealth, especially with appreciating assets like real estate. However, high-interest consumer debt is a wealth killer. I once advised a family carrying $50,000 in credit card debt while simultaneously trying to invest. We focused on aggressively paying off that debt first. This freed up cash flow that we then redirected to long-term investments. This seemingly simple change supercharged their progress.

This brings us to cash flow management. It’s not just about budgeting; it’s about aligning your spending with your generational goals. Prioritize investments that compound over time, while still enjoying your current lifestyle. It’s a tricky balance, but it’s crucial for building lasting wealth.

Trust Strategies That Work In Real Life

Trusts are a hot topic in generational wealth planning these days, but choosing the wrong one can really cost you. I've seen it happen – a trust can be a lifesaver for one family and a bureaucratic nightmare for another. The real secret? Picking a structure that actually works for your family's unique needs, not just the size of your assets. Let's look at how this plays out in the real world.

Choosing the Right Trust Structure

A revocable living trust offers solid basic protection and keeps you in control. Plus, it helps you avoid probate, which can be a huge time and money saver. For many families, this is a perfect starting point. But for more complex situations, a dynasty trust might be a better fit. This type of trust is designed for passing down wealth across multiple generations, potentially shielding your assets for decades to come.

I once worked with a family who managed to save a whopping $3 million in estate taxes. Their secret weapon? A relatively straightforward grantor retained annuity trust (GRAT). They were able to transfer future asset growth to their children while minimizing the tax hit. The takeaway here isn’t about making things complicated, it's about using the right tool for the job.

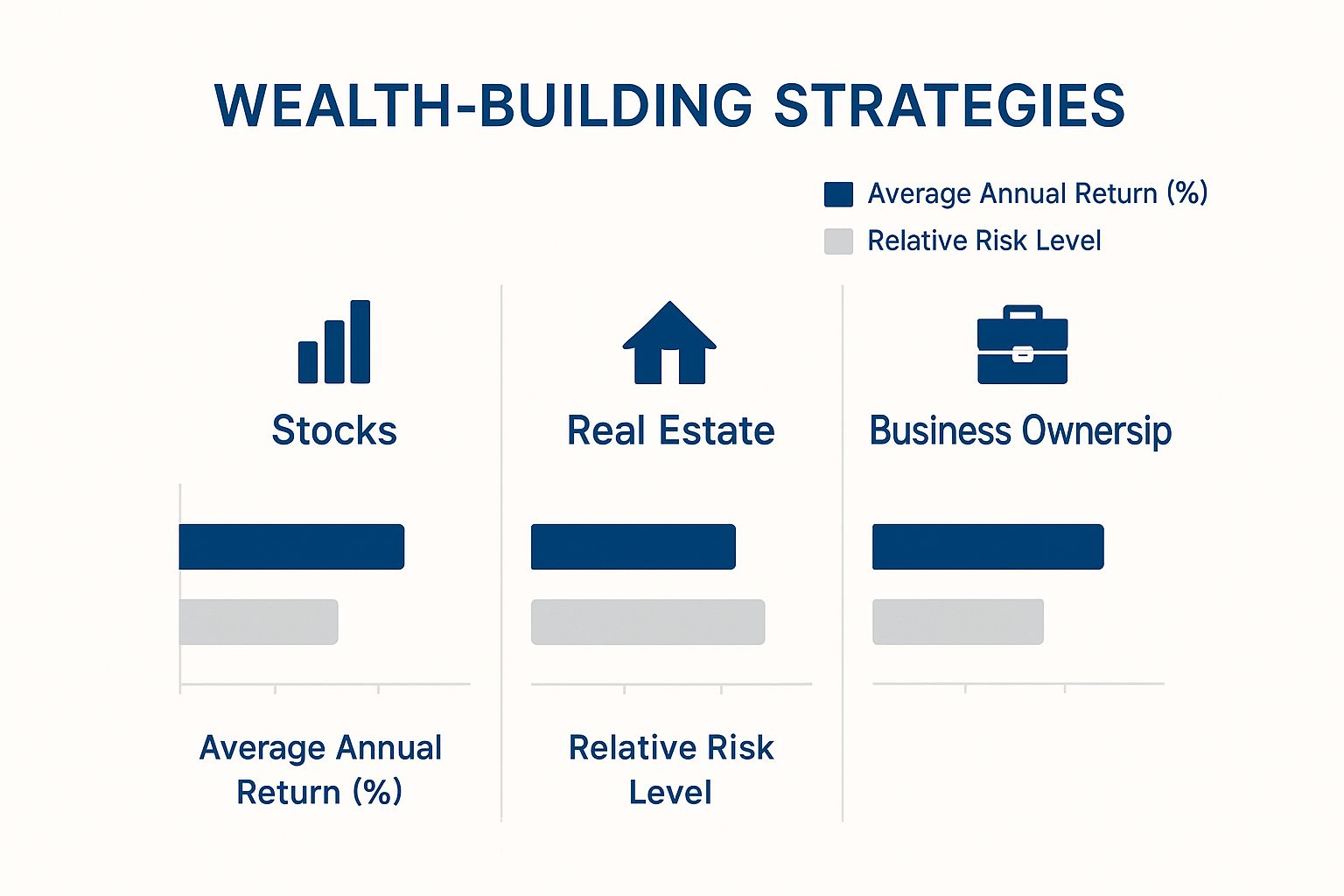

Speaking of the right tools, take a look at this infographic. It breaks down the average annual returns and relative risk levels of three common wealth-building strategies: stocks, real estate, and business ownership.

As you can see, business ownership can bring high returns, but it’s also riskier. Stocks land somewhere in the middle, and real estate, while generally offering lower returns, is often seen as a safer bet. Getting a handle on these dynamics is crucial for any successful generational wealth plan.

To help you even further in choosing the right strategy, I've put together this handy comparison guide:

Trust Strategy Comparison Guide: Side-by-side comparison of popular trust types with their benefits, costs, and ideal use cases

Trust Type | Tax Benefits | Control Level | Complexity | Best For |

|---|---|---|---|---|

Revocable Living Trust | Avoids probate, potentially reducing estate taxes | Grantor maintains full control | Relatively simple | Basic estate planning, avoiding probate |

Dynasty Trust | Potential for significant estate and generation-skipping transfer tax savings | Less control for grantor after creation | Complex | Multi-generational wealth transfer |

Grantor Retained Annuity Trust (GRAT) | Minimizes gift tax on transfer of appreciating assets | Grantor receives annuity payments | Moderate complexity | Transferring future asset growth |

Charitable Remainder Trust | Income tax deductions, reduced estate taxes | Grantor receives income stream | Moderate complexity | Philanthropic giving, lifetime income |

This table highlights the key differences between various trust types, allowing you to easily compare their benefits and drawbacks. Choosing the right trust depends heavily on your individual goals and circumstances, so consulting with a financial advisor is always recommended.

Avoiding Common Trust Pitfalls

One thing I always stress is understanding the difference between grantor trusts and non-grantor trusts. They have different tax implications, which can make a big difference down the road. Grantor trusts are generally simpler to manage and offer some tax advantages, while non-grantor trusts are more complex but can provide better asset protection.

Another potential pitfall is overcomplicating things. Generation-skipping strategies can be incredibly useful, but they aren’t always the answer. I’ve seen families create overly complex dynasty trusts that ended up causing more problems than they solved. For example, a business owner I worked with was able to successfully exit his company using a charitable remainder trust. This strategy not only gave him lifetime income but also benefited his favorite charity – a win-win!

Remember, generational wealth planning isn't just about building a fortune; it's about ensuring that wealth reaches the next generation. It's about building a lasting legacy. Take the time to really consider your family's specific needs and choose the trust strategy that aligns with your long-term goals. Don’t let the appeal of complex strategies distract you from practical, effective solutions.

Tax Planning Without Triggering Audits

Let’s be honest, nobody loves talking about taxes. But they’re absolutely essential to any serious generational wealth plan. Get your tax strategy right, and you could save your family millions. Get it wrong, and… well, let’s just say audits aren’t fun. The real secret? Working with the tax code, not trying to fight it. I’ve seen families win big and lose big, and the winners always focus on smart, legitimate strategies.

The Power of Gifting

One of the most effective strategies I’ve seen is surprisingly simple: annual gifting. You can gift a certain amount each year to as many people as you like, completely tax-free. This lets you gradually transfer wealth over time, especially if those gifts are then invested for growth. I know one family who strategically gifted $10 million to their children over several years using annual exclusions. Zero gift tax. It’s all about understanding the rules and using them to your advantage.

GRATs and Charitable Strategies

For larger estates, a grantor retained annuity trust (GRAT) can be incredibly powerful. A GRAT lets you transfer the growth of assets, minimizing gift tax. I worked with a family who saved $2 million in taxes with a well-structured GRAT. But here’s the thing: GRATs are complex. Don’t try to DIY this one. Get expert advice and make sure it fits your overall generational wealth plan. It’s not a one-size-fits-all solution.

And don’t forget the power of charitable giving. It’s not just about doing good; it can also have significant tax benefits. Charitable remainder trusts and charitable lead trusts are just two examples of how you can give back and benefit your family's financial future at the same time.

Avoiding Tax Traps

I’ve seen some families try to get too clever with taxes, leading to audits and penalties that wiped out any potential gains. One common mistake? Trying to hide assets or income. The IRS is much more sophisticated than you think. The consequences can be devastating. Remember, building generational wealth is a marathon, not a sprint. Focus on building sustainable, legally sound strategies for long-term success. Avoid schemes that promise quick wins. They often lead to long-term losses. Slow and steady wins the race.

Investment Thinking For Multiple Generations

Building wealth that lasts generations takes a different mindset than simply planning for your own retirement. When your horizon stretches 50+ years instead of 20, everything changes. Your risk tolerance, how you diversify, even your definition of a "good" return – it all takes on a new meaning. I've spent time with family office managers who've successfully navigated multiple market cycles, and their strategies are a far cry from typical financial advice.

Long-Term Portfolio Construction

So, how do these families build portfolios designed to benefit generations yet to be born? They often look beyond the usual stocks and bonds and consider alternative investments. Think private equity, real estate, and even some niche areas most advisors wouldn't touch. I've seen families invest in things like farmland, timber, and even fine art. You won't find these in your average 401(k), but they offer distinct ways to grow and protect wealth over the very long haul. Plus, these unique investments can be a fantastic learning experience for younger family members, giving them a tangible connection to the family’s legacy.

Traditional asset allocation models like the 60/40 stock/bond split might work for retirement, but they’re often too shortsighted for multi-generational planning. Families with a long view understand they can weather market storms and grab opportunities that just wouldn’t make sense for short-term investors. This long-term perspective shapes every single investment decision. And speaking of changing priorities, global surveys of high-net-worth individuals reveal interesting trends. The 2025 EY Global Wealth Research Report, which surveyed nearly 3,600 wealthy clients across over 30 countries, found that intergenerational wealth transfer is a major concern shaping how families manage their finances. You can dig into their findings here.

Balancing Growth and Education

One family I know has a really interesting approach. They've structured a portion of their portfolio for impact investing. This lets younger family members choose projects that align with their values. It's not just about financial returns; it’s also a powerful way to teach future generations about responsible wealth management and making a positive social impact. That kind of hands-on experience is incredibly valuable. Even just including the younger generation in investment discussions, even in small ways, can build financial literacy and a sense of shared responsibility.

Real-World Portfolio Examples

Looking at real-world portfolios reveals how families balance current income needs with long-term growth objectives. Some prioritize consistent cash flow through dividend-paying stocks or rental properties. This covers current expenses and allows the core portfolio to appreciate over time. Others might lean heavily into growth assets, accepting more short-term volatility for potentially bigger gains down the road. There's no one-size-fits-all approach. The key is to develop a clear strategy that matches your family’s specific values and goals. Interestingly, some of the most successful generational wealth builders make choices that would make a typical financial advisor raise an eyebrow. They understand that conventional wisdom doesn’t always apply when you're playing the ultra-long game. They're comfortable with calculated risks and exploring unconventional opportunities that others might overlook. This willingness to think differently is often what separates those who build true, lasting wealth from the rest.

Raising Heirs Who Don't Blow Everything

Let's face it, money can disappear fast without a good head on your shoulders. I've seen it happen too often: families pour all their energy into the technical side of generational wealth planning – trusts, investments, and the like – but completely forget about the most important piece of the puzzle: the kids. They end up raising entitled children who view the family fortune as a free pass, not a responsibility. The families who really nail this whole generational wealth thing understand one key truth: preparing your heirs is just as critical as your investment strategy.

Financial Education That Actually Works

So, how do you raise kids who are responsible with money? It all starts with talking about finances in a way they can understand, starting at a young age. I'm not talking about formal lectures, but rather weaving financial concepts into everyday life. Think about it: including your kids in simple budgeting decisions or explaining why you chose one item at the grocery store over another (because of value, needs vs. wants, etc.) can build a fantastic foundation for smart money habits later on.

Giving older children an allowance tied to chores or responsibilities can also be hugely beneficial. This helps them grasp that connection between effort and reward, setting them up for financial independence. It’s not just about handouts; it’s about teaching them the value of a dollar.

Governance and Family Harmony

Families who successfully pass down wealth often create structures to minimize conflict, too. A well-defined family mission statement can be a game changer. Think of it as a constitution for your family’s wealth. It acts as a guide for decision-making, keeping everyone aligned on the big picture. This might include outlining shared values and how you, as a family, will use resources to achieve those goals. This simple step can prevent so many headaches – and resentments – down the road.

For example, your mission statement might prioritize education, charitable giving, or supporting family-owned businesses. By clearly stating these priorities, you’ll find it much easier to make financial decisions that reflect what your family truly values.

Encouraging Contribution, Not Consumption

The ultimate goal isn't to control the next generation but to empower them. This means instilling a sense of contribution, not just allowing them to be consumers. I’ve worked with families who insist their children earn their own money, even if a significant inheritance is on the horizon. This builds a strong work ethic and a sense of self-reliance that money can’t buy.

One family I know requires their adult children to work outside the family business for a few years before joining. This gives them invaluable outside perspective and helps avoid a sense of entitlement. Another family I’ve worked with has a matching program for charitable donations, encouraging philanthropy from a young age. These are just a couple examples, but the point is to raise thoughtful stewards of wealth, not just heirs waiting for a payout. It's about instilling values and giving them the tools to use their resources to make a real difference in the world.

Your Practical Generational Wealth Action Plan

Okay, so you've learned a lot about building generational wealth. The biggest pitfall? Trying to do too much at once. It just gets complicated and you don't see real results. A better way is to be systematic, focusing on the most impactful strategies first. Whether your family is just starting out or ready for more advanced moves, there's a roadmap for you.

Building Your Action Plan, Step by Step

Building generational wealth isn’t just for millionaires. It's a mindset. It's about thinking generationally from the very beginning, creating a plan that fits your family’s unique situation. Here’s how to get started:

Assess your current situation: Take an honest look at your finances. What assets do you have? What debts? What’s coming in and what’s going out? This gives you a starting point.

Define your goals: What does generational wealth actually mean to your family? Is it about paying for education? Supporting a family business? Leaving a philanthropic legacy? Get specific.

Prioritize strategies: Now, based on your goals, pick the strategies that will have the most impact. Maybe that’s starting annual gifting. Maybe it's finally getting your estate plan in order. Don’t try to do everything at once!

Assembling Your Advisory Team

You're going to need a good team. Think of it like assembling your own personal financial A-Team. You’ll want a financial advisor, an estate planning attorney, and a tax professional. Don't just pick the first names you find. Look for advisors who really get generational wealth planning and whose values align with your family’s. Here's a pro-tip: ask other families who have successfully built legacies for their recommendations. This can save you a ton of time and prevent costly mistakes down the road.

Family Meetings That Matter

Regular family meetings about finances are important, but they need to be effective. Have a clear agenda, focus on specific decisions, and make sure everyone feels heard. I know one family who uses these meetings to teach their kids about the family finances. They talk about investments, charitable giving, even the family business. It’s a fantastic way to bring younger generations into the conversation and build a shared understanding of the family's financial goals.

Tracking Your Progress

How will you know if you're on track? Set clear benchmarks and track your progress regularly. This could be anything from the value of your investments to how many assets you've transferred to the next generation. A simple but powerful tool is a family balance sheet. This shows you, at a glance, your assets and liabilities, giving you a clear picture of your overall financial health.

Accountability and Momentum

Accountability is huge for long-term success. Share your goals with a trusted advisor or family member – someone who will keep you on track. And don't forget to celebrate your wins along the way! Acknowledging your progress reinforces good habits and builds momentum that compounds over time. Building generational wealth isn’t a sprint; it’s a marathon. Start with intention, not just money.

Ready to secure your family's future and create a legacy that lasts? Explore the comprehensive, value-driven insurance options available at America First Financial and start planning for generations to come.

Comments