_edited.png)

Term Life Insurance for Families | Protect What Matters Most

- dustinjohnson5

- May 10, 2025

- 12 min read

Demystifying Term Life Insurance For Modern Families

Term life insurance often forms the foundation of a solid family financial plan. This type of insurance provides a death benefit to your beneficiaries if you die within a specific period, or term. These terms typically range from 10, 20, or 30 years. Understanding its core purpose—providing temporary but vital coverage—is the first step to understanding this important financial tool.

Why Term Life Insurance Is A Family Favorite

Term life insurance often makes the most sense for families because it aligns with periods of significant financial responsibility. It can cover the years your children are financially dependent or while you're paying off a mortgage. This allows you to secure a substantial death benefit at a much lower cost than permanent life insurance. The simplicity of term life insurance also adds to its appeal. You pay a predictable premium for a set period, making budgeting and financial planning easier.

How Term Life Insurance Works In Practice

Think of term life insurance as a safety net for a specific period. You choose the term length and coverage amount based on your family's needs. If you die during the term, your beneficiaries receive the death benefit. This payout can replace lost income, pay off debts (like a mortgage), cover education expenses, or provide financial security for your family's future. If you outlive the term, the coverage expires. This straightforward structure makes term life insurance accessible and affordable.

Term Life Insurance Growth And Trends

Term life insurance has long provided financial security for families worldwide. The market has seen ups and downs, but experienced a rebound in 2023 due to the expansion of digital platforms and competitive pricing. This growth, particularly strong in the U.S., occurred despite economic challenges like inflation and rising interest rates. Looking ahead, experts project moderate growth of 1% to 5% for term life insurance premiums in 2025. Explore this topic further here. This anticipated growth highlights the continuing importance of term life insurance in providing financial security for families.

Why Your Family Deserves This Financial Safety Net

Protecting your family's financial future is a fundamental concern for most parents. Term life insurance acts as a crucial safety net, providing a financial cushion during critical family-building years. It's not just about having coverage; it's about the peace of mind that comes from knowing your loved ones are protected, regardless of life's uncertainties.

Securing Your Family’s Future

Thinking about real-life scenarios helps illustrate why term life insurance for families is so essential. Imagine the impact of losing a primary income earner. How would the mortgage be paid? Would there be enough money for your children's education? Term life insurance offers solutions by providing a death benefit. This benefit can replace lost income, ensuring your family maintains their standard of living.

Navigating Life’s Transitions With Confidence

Life is full of transitions: new babies, home purchases, career changes, and caring for aging parents. Each stage brings unique financial challenges. Term life insurance adapts to these changes, offering flexible protection as families navigate these milestones. It allows families to focus on enjoying these transitions, instead of worrying about the financial implications. For instance, the death benefit could cover childcare costs after a new baby arrives or support elderly parents.

The Psychological Benefits of Protection

The financial safety net of term life insurance also provides significant psychological benefits. Knowing your loved ones are protected can reduce stress and anxiety. This allows you to focus on what truly matters: spending time with your family and enjoying life. This peace of mind is priceless, especially during difficult times.

Real-World Impact: From Difficulty to Security

Many families have learned the hard way about the difference between adequate and inadequate life insurance coverage. There are countless stories of families struggling financially after an unexpected loss, barely able to meet their basic needs. Proper term life coverage, however, can prevent difficult situations from becoming financial catastrophes. The growth of the global life insurance market highlights this growing need for security. In 2024, the global market reached $3.1 trillion, with life premiums in advanced markets projected to grow by 1.5% through 2025. Find more detailed statistics here. This growth reflects a greater understanding worldwide of the importance of financial protection and stability for families.

More Than Just a Policy, It’s Peace of Mind

Ultimately, term life insurance for families is about more than just finances. It’s about ensuring your family’s well-being and providing a secure foundation for their future. It demonstrates your love and commitment, offering your family the gift of financial security and the freedom to thrive.

Calculating Coverage That Actually Protects Your Family

Determining the right amount of term life insurance for your family requires careful consideration. It's about more than just your current income. You also need to assess your debts, future expenses, and long-term financial goals. This comprehensive view will help you determine the coverage that truly protects your family's future. When calculating coverage, also consider specialized needs such as insuring items in storage.

The DIME Method: A Practical Framework

Financial planners often use the DIME method to calculate appropriate coverage. DIME stands for Debt, Income, Mortgage, and Education. This framework provides a structured way to assess what your family would need if you were to unexpectedly pass away. By breaking down your financial obligations into these four key areas, you can create a more accurate estimate of your coverage needs.

Debt: Include all outstanding debts such as credit cards, loans, and other liabilities.

Income: Calculate the income replacement your family would need. Consider a timeframe of 5, 10, or even 20 years of your current salary.

Mortgage: Factor in your mortgage balance to ensure it can be paid off, relieving your family of that burden.

Education: Estimate the future cost of your children's education, including everything from kindergarten through college.

Life Stages and Coverage Needs

As your family grows and changes, so will your insurance needs. A young family with a mortgage and young children has different needs than a family approaching retirement. Regularly reviewing your coverage ensures it aligns with your current circumstances.

New Parenthood: Focus coverage on income replacement, debt payoff, and childcare costs.

Growing Families: Consider increasing coverage as your family expands and expenses increase.

College Planning: Include future tuition costs and other education-related expenses.

Nearing Retirement: Coverage might decrease as debts are paid and children become financially independent.

To further illustrate how coverage needs vary across life stages, consider the following table:

Family Protection Calculator: Coverage Needs Across Life Stages This table helps families determine appropriate term life insurance coverage amounts based on different family structures and financial situations.

Family Type | Recommended Coverage Range | Key Considerations | Additional Protection Needs |

|---|---|---|---|

Single, No Dependents | 1-3x Annual Income | Debt repayment, funeral expenses | - |

Young Couple, No Children | 5-7x Annual Income | Joint debts, future plans (e.g., home purchase) | Disability insurance |

Family with Young Children | 10-12x Annual Income | Mortgage, childcare, education expenses | Critical illness insurance |

Family with Teenage Children | 8-10x Annual Income | College savings, ongoing living expenses | Long-term care insurance (for aging parents) |

Empty Nesters/Nearing Retirement | 5-7x Annual Income | Remaining mortgage, travel plans | Estate planning |

This table provides general guidelines. Individual circumstances vary, so consulting with a financial advisor is crucial for personalized advice.

Avoiding Common Coverage Mistakes

Underestimating future needs is a common mistake. Inflation can significantly reduce a death benefit's value over time. Also, failing to account for changes like a new child or a spouse leaving the workforce can leave your family underprotected. Regularly reviewing and adjusting your policy is essential.

Ensuring Complete Protection

To maximize your term life insurance, use straightforward calculations. Account for potential inflation when determining income replacement needs. Regularly reassess your family's financial situation and adjust your coverage accordingly. By proactively managing your policy, you can ensure continuous, adequate protection. This secures your family’s financial future.

Finding Your Family's Perfect Term Life Insurance Match

Not all term life insurance policies are the same. Understanding the nuances of coverage is vital for families. This means looking beyond confusing insurance terminology and focusing on how different policies address your family's actual needs. Let's explore how factors like term length, policy features, and optional riders can affect your family's financial well-being.

Matching Term Length to Life Stages

The policy term, or the length of time your coverage lasts, should align with your family’s financial obligations. A shorter, 10-year term might be suitable for a car loan or other smaller debt. However, a 20- or 30-year term often makes more sense for longer-term commitments like a mortgage or your children's education. Choosing the right term length is about matching protection to your family's current and future financial landscape.

Essential Policy Features for Families

Some policy features are more important than others for families. A convertibility option, which allows you to convert your term policy to a permanent one, provides flexibility as your needs change over time. Riders, such as a waiver of premium for disability, add extra security during challenging circumstances. Understanding which features genuinely enhance your coverage and which only increase the cost without adding significant value is crucial. Carefully consider whether a 10-year term with renewal options might be a better choice than a 30-year policy based on your individual needs and financial situation.

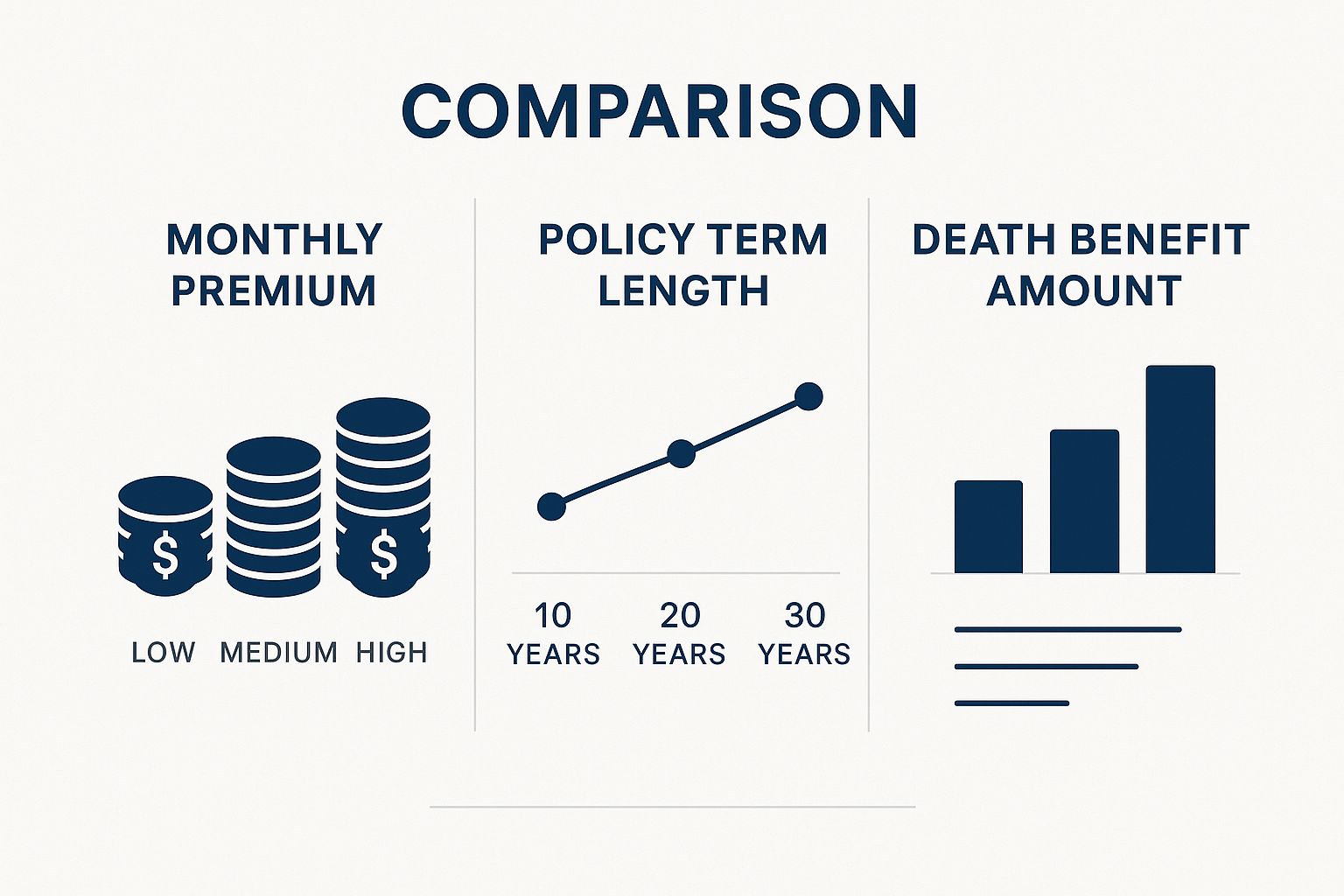

The infographic below illustrates how monthly premiums, policy term length (10, 20, and 30 years), and death benefit amounts all relate to one another to create different policy options.

As the infographic shows, longer policy terms and higher death benefits generally lead to higher monthly premiums. The optimal balance depends on your family's budget and the level of coverage you require.

To help families compare and select the right term life insurance, the following table provides a detailed overview of different options:

Family-Focused Term Life Policy Comparison Guide

This table compares different term life insurance options to help families select the most appropriate coverage for their needs.

Term Length | Best For | Typical Premium Range | Key Benefits | Potential Drawbacks |

|---|---|---|---|---|

10 Years | Short-term debts (car loans, personal loans) | Lower | Lower initial cost, good for specific needs | Coverage expires after 10 years, might not cover long-term needs like mortgage or children's education |

20 Years | Covering a mortgage, children's education | Moderate | Balances cost and coverage duration | Higher premiums than 10-year term |

30 Years | Long-term financial protection, estate planning | Higher | Longest coverage period, provides security throughout key financial stages | Highest premiums, might be unnecessary if shorter term fulfills needs |

This comparison highlights how different term lengths align with specific financial goals, allowing families to choose the balance of coverage and affordability that suits them best. While a 10-year term offers a lower initial cost, a 30-year term provides the most extensive coverage, though at a higher price.

Navigating the Term Life Insurance Market

The term life insurance market remains a complex environment, especially for families. The U.S. individual life insurance market has remained relatively stable even with economic changes. For example, group life insurance sales experienced an 8% year-over-year increase in the fourth quarter of 2023, with an annual growth rate of 6% for the entire year. Term life insurance is still a primary choice for families seeking affordable coverage. Competitive pricing and digital platforms are increasing accessibility for consumers. Learn more about insurance industry trends here.

Balancing Protection and Cost

Finding the right term life insurance means balancing comprehensive protection with a price you can afford. This involves understanding your family's unique needs and selecting a policy that meets those needs without unnecessary additions. Carefully evaluating term length, essential policy features, and understanding the market landscape will allow you to ensure your family's financial security.

Smart Strategies for Affordable Family Protection

Securing robust term life insurance for your family doesn't have to be a financial burden. Many families use smart strategies to get the coverage they need at a price they can afford. By understanding the factors that affect premiums and using some planning techniques, you can find a good balance between protection and affordability.

Understanding the Pricing Levers

Several factors influence your term life insurance premiums. Think of these as "pricing levers" that can be adjusted to find a policy that fits your budget. Your age is a significant factor, with younger applicants typically qualifying for lower rates. Health status also plays a key role. Insurers use health classifications based on your medical history and lifestyle. A better health classification generally results in lower premiums.

The policy structure itself also impacts cost. Longer terms, such as a 30-year policy, have higher premiums than shorter terms like 10 or 20 years. The death benefit amount you select directly affects the premium. A higher death benefit will mean a higher premium.

Techniques for Balancing Protection and Cost

Financial advisors often recommend strategies like coverage layering and policy stacking. Coverage layering involves combining different insurance types, such as a smaller permanent policy with a larger term policy. This approach offers lifelong coverage and cost-effective protection during critical periods. Policy stacking uses multiple smaller term policies with staggered expiration dates to meet specific financial goals, potentially offering premium savings over time.

Cost Breakdowns: Factors That Influence Your Premium

Beyond age and health, lifestyle choices and policy features affect premium calculations. Smoking significantly increases rates. Dangerous hobbies can impact your insurability and price. Certain riders, which offer additional benefits such as waiver of premium for disability, add to the overall cost.

Insider Tips for Securing Competitive Rates

Working with an independent agent allows you to compare quotes from multiple insurers to find the best rates. Timing your application strategically, such as before major life events like marriage or starting a family, can help secure lower premiums. If you’ve made health improvements, like quitting smoking or losing weight, reapplying for insurance may lead to a better health classification and lower premiums.

Realistic Premium Expectations

Premiums vary significantly based on individual circumstances. A healthy 30-year-old non-smoker seeking a $500,000, 20-year term policy might expect to pay between $25 and $50 monthly. A 45-year-old smoker with the same coverage could pay substantially more. Consulting an agent or using online quote tools from insurers like America First Financial can give you more personalized estimates.

Maximizing Coverage, Minimizing Cost

Protecting your family doesn't require choosing the most expensive policy. By understanding the pricing factors and exploring different strategies, you can find affordable term life insurance that meets your needs without unnecessary extras. Evaluate your needs, compare quotes, and consider options like coverage layering or policy stacking to optimize your family’s financial protection.

Navigating the Application Journey With Confidence

Applying for term life insurance for your family doesn't have to be a daunting task. By understanding the process and preparing in advance, you can navigate the application with confidence. This section will break down each step, highlighting key information and clarifying potential concerns.

Understanding the Underwriting Process

Underwriting is the process insurance companies use to assess your risk and determine your premiums. Factors such as your age, health history, lifestyle, and occupation are all considered. This information helps them categorize you into different risk levels, influencing your health classification and the ultimate cost of your coverage. Proper preparation for this process is essential for securing the most favorable outcome.

Preparing for Medical Examinations

Some policies require a medical exam. While this might seem intimidating, being prepared can reduce stress and potentially improve your health classification. Be honest and transparent about your medical history. Avoid caffeine and alcohol before the exam, and ensure you're well-rested. This allows you to present an accurate picture of your health.

Application Shortcuts: Simplified Issue vs. Traditional Underwriting

Simplified issue policies offer a streamlined application process, often waiving the medical exam requirement. These policies are a suitable option for families looking for quick coverage, especially if they're in good health. However, traditional underwriting, while requiring a medical exam, can offer lower premiums long-term, especially for healthy individuals. The right choice depends on your family’s specific needs and priorities.

Handling Special Situations

Pre-existing conditions, high-risk hobbies, or complex family structures can introduce additional complexity to the application process. Be ready to provide supplementary information or documentation. In these situations, working with an experienced insurance agent can be especially beneficial. An agent can provide expert guidance and advocate for your best interests throughout the application process.

Tips for a Smooth Application

Gather necessary documents: Compile relevant documents such as medical records, financial statements, and identification in advance.

Answer health questions accurately: Providing accurate and complete information is critical. Inaccurate information can potentially lead to claim denials later.

Understand the timeline: The application process can typically take several weeks depending on the policy type and underwriting process. Be prepared for this timeframe to avoid unnecessary anxiety.

By following these steps and gaining a thorough understanding of the underwriting process, you can make well-informed decisions and provide accurate information, leading to a more efficient application process. This proactive approach increases your chances of securing the most favorable terms for your family's term life insurance policy.

Maximizing Your Family's Term Life Insurance Value

Your term life insurance policy isn't a static purchase; it's a dynamic partnership requiring regular attention to ensure it aligns with your family's changing needs. Just as families grow and evolve, so should their insurance coverage. This section explores strategies for getting the most out of your policy.

Regular Policy Reviews: Adapting to Life's Changes

Life is a journey filled with significant milestones: marriages, births, new jobs, and even moving to a new city. Each of these events can significantly alter your family's financial landscape and, therefore, your term life insurance needs. Regular policy reviews, especially after major life events, are crucial. For example, welcoming a new child might mean you need more coverage, while a substantial salary increase could allow you to adjust your existing policy.

Managing Renewals, Conversions, and Adjustments

As your term policy's expiration date approaches, you'll need to decide whether to renew, convert, or seek entirely new coverage. Understanding your options is essential. Renewing might be convenient, but it could mean higher premiums due to your age. Converting your term policy to a permanent one provides lifelong coverage, but at a greater cost. Exploring new term policies from different insurers can be a way to find competitive rates, especially if you're healthier now than when you first applied. The application process itself can seem complex, some companies like SpringVerify have made background verification checks more efficient.

Beneficiary Designations and Policy Riders

Regularly review your beneficiary designations—the people who will receive the death benefit—and update them as necessary. This ensures the intended individuals are protected. Also, take the time to understand your policy riders. These optional additions can significantly enhance your coverage. For example, a waiver of premium rider ensures your premiums are paid if you become disabled.

Beyond the Death Benefit: Maximizing Policy Benefits

Term life insurance often offers advantages beyond the death benefit itself. Some policies provide access to accelerated death benefits for terminal illnesses, providing financial relief during difficult times. Understanding all aspects of your policy allows you to take full advantage of its features.

Transitioning to New Coverage Solutions

As your term nears its end and your family's circumstances change, transitioning to a new coverage plan may be necessary. This could involve considering other types of life insurance, such as permanent life insurance, or modifying your current term coverage to better reflect your financial situation. Proactive planning for this transition ensures your family's ongoing protection.

Ready to protect your family's future? Get a free quote from America First Financial in under three minutes and discover how we can help you safeguard what matters most.

Comments