_edited.png)

Top 7 Alternatives to Obamacare You Should Know

- dustinjohnson5

- Apr 30

- 19 min read

Beyond Obamacare: A Look at Healthcare Options

Looking for healthcare alternatives to Obamacare? This listicle explores seven key options, from Medicare for All to market-based reforms, to help you understand the potential benefits and drawbacks of each. Whether you prioritize affordability, comprehensive coverage, or state-based solutions, understanding these alternatives is crucial for making informed decisions about your family's healthcare. This guide provides valuable insights into options beyond the Affordable Care Act, empowering you to choose the best path forward.

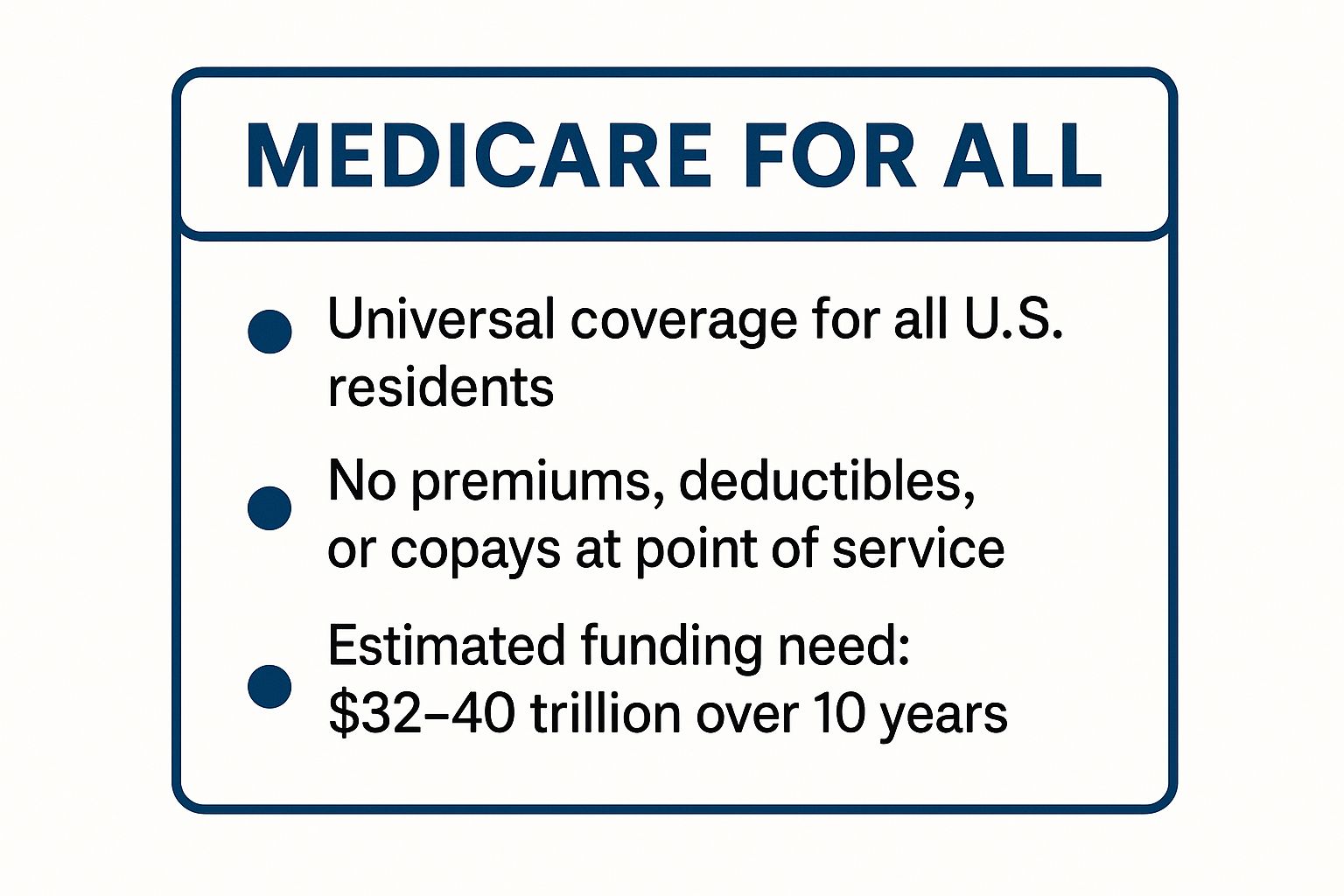

1. Medicare for All

As an alternative to the Affordable Care Act (Obamacare), "Medicare for All" proposes a fundamental shift in how healthcare is delivered and financed in the United States. This system envisions a single-payer, national health insurance program covering every American, effectively replacing private insurance, Medicare, Medicaid, and other existing public health programs. The core principle is to eliminate the complex web of insurance companies, premiums, deductibles, and co-pays, replacing it with a streamlined, publicly funded system financed through taxes.

The infographic above summarizes the key aspects of Medicare for All: universal coverage, elimination of private insurance, comprehensive benefits, no out-of-pocket costs at the point of service, and government negotiation of healthcare prices. This visualization highlights the potential for simplified healthcare financing and cost control through bulk purchasing power. However, it also underscores the significant shift away from the current private insurance-based system.

Medicare for All aims to provide comprehensive benefits, including dental, vision, and long-term care, services often excluded from standard insurance plans. The government would negotiate prices with healthcare providers and pharmaceutical companies, theoretically driving down costs and ensuring affordable access to care for all. While proponents argue this system would simplify healthcare and eliminate medical bankruptcies, critics express concerns about potential tax increases and the impact on the existing healthcare industry.

Here's a quick reference summarizing the key features of Medicare for All:

Universal Coverage: All U.S. residents are covered, regardless of pre-existing conditions, employment status, or income.

No More Private Insurance: Private health insurance companies are eliminated, with the government becoming the sole payer.

Comprehensive Benefits: Includes hospital stays, doctor visits, prescription drugs, mental health services, dental, vision, and long-term care.

No Out-of-Pocket Costs: Eliminates premiums, deductibles, and co-pays at the point of service.

Government Price Negotiation: The government negotiates prices with healthcare providers and pharmaceutical companies to control costs.

This summary helps us bridge to examining the potential advantages and disadvantages of this system, particularly for specific demographics like conservative American families, individuals approaching retirement, health-conscious consumers, budget-minded insurance shoppers, and patriotic individuals.

Pros:

Peace of Mind: Universal coverage provides security, ensuring access to necessary care regardless of job loss or changing financial circumstances. This is particularly beneficial for families and those approaching retirement.

Simplified System: Eliminates the complexities of navigating multiple insurance plans, premiums, and deductibles, offering a streamlined approach to healthcare.

Cost Control (Potentially): Government negotiation of prices could lower healthcare costs, appealing to budget-minded individuals and families.

Focus on Health Outcomes: By removing financial barriers, the focus shifts towards preventative care and overall health improvement, appealing to health-conscious consumers.

Cons:

Tax Increases: Funding a universal healthcare system requires substantial tax increases, a potential concern for fiscal conservatives and families.

Potential Wait Times: Critics argue a single-payer system could lead to longer wait times for certain procedures due to increased demand.

Disruption to Existing Industry: The elimination of private insurance companies would cause significant disruption to the healthcare industry and potential job losses.

Impact on Innovation: Some argue government control could stifle innovation in the healthcare sector.

Government Control: Increased government involvement in healthcare could be a concern for some, especially those who value individual liberty and limited government.

Medicare for All is a radical departure from the current U.S. healthcare system. While examples of similar systems exist in other countries like Canada and the United Kingdom, implementing such a system in the U.S. would be a complex undertaking with both potential benefits and drawbacks. Understanding these complexities is crucial for informed decision-making, particularly for conservative American families, those nearing retirement, and budget-conscious individuals. Currently, there is no direct website for a national Medicare for All program as it hasn't been implemented in the US. However, organizations like Physicians for a National Health Program (PNHP) provide more information on this proposed system. This alternative to Obamacare deserves consideration due to its potential to address affordability and access issues, but it's essential to weigh the potential costs and consequences carefully.

2. Public Option

For those seeking alternatives to Obamacare, the Public Option presents a compelling path towards more affordable and accessible healthcare. It proposes a government-run health insurance plan that would compete directly with private insurance companies on the marketplace. This approach maintains the existing multi-payer system, a key difference from single-payer systems, while introducing a public alternative designed to increase competition and potentially drive down costs for consumers. This resonates particularly well with budget-minded insurance shoppers and those approaching retirement, who are often on fixed incomes and sensitive to healthcare expenses.

The Public Option allows individuals to choose between a government-administered plan or a private plan. While premiums and cost-sharing would still exist under the public option, they are projected to be potentially lower than private insurance due to the government's negotiating power with healthcare providers. This added competition could incentivize private insurers to lower their premiums as well, benefiting consumers across the board. This aspect appeals to conservative American families who value choice and competition in the marketplace and are wary of government monopolies.

Several states have already begun exploring public option programs, providing valuable insights into potential benefits and challenges. Washington state's Cascade Care, Colorado's public option program, and Nevada's public option legislation serve as real-world examples of how a public option can be implemented. These programs offer valuable case studies for other states considering similar initiatives, demonstrating the public option's potential within the current healthcare landscape. These examples also demonstrate a path toward reform that doesn't involve a complete overhaul, potentially appealing to those who are wary of drastic changes.

Actionable Tips:

Research your state's healthcare landscape: Look into whether your state is considering or has implemented a public option program.

Compare potential costs: If a public option is available, compare premiums, deductibles, and co-pays with your current private insurance plan.

Consider your healthcare needs: Evaluate whether the coverage offered by a public option plan meets your specific healthcare requirements.

When and Why to Use This Approach:

The Public Option is a worthwhile alternative to Obamacare for those who:

Are struggling with high private insurance premiums.

Desire more choice and competition in the health insurance market.

Prefer a less disruptive approach to healthcare reform than a single-payer system.

Want a safety net option in case they are unsatisfied with private insurance offerings.

Pros:

Less disruptive to the current system than single-payer, appealing to conservative values.

Increased competition can lower premiums, a significant benefit for budget-minded individuals.

Provides a safety net and choice for consumers.

Potential for expanded coverage to uninsured populations.

More politically feasible than a complete system overhaul.

Cons:

May not achieve universal coverage.

Possibility of adverse selection if primarily high-risk individuals enroll.

Continued complexity in healthcare administration.

Potential for opposition from the healthcare industry.

Effectiveness hinges on implementation details.

The Public Option offers a pragmatic approach to healthcare reform, balancing the need for affordability and accessibility with a commitment to maintaining a degree of private market competition. It deserves a place on this list as a viable alternative to Obamacare, particularly for those seeking more affordable options and a more gradual approach to healthcare system change. It's an option worth exploring for those who prioritize choice and competition, a key tenet for many conservative American families and patriotic individuals.

3. Market-Based Reforms

Market-based reforms offer a distinct alternative to Obamacare, emphasizing consumer choice, competition, and free-market principles to drive down healthcare costs and improve quality. This approach seeks to minimize government intervention and empower individuals to make informed decisions about their healthcare. Instead of relying on mandates and subsidies, market-based reforms focus on creating a more transparent and competitive healthcare marketplace where consumers can shop for plans that best suit their needs and budgets. This approach often includes strategies like expanding Health Savings Accounts (HSAs), promoting interstate insurance sales, requiring price transparency, and reducing regulations on insurers.

For conservative American families, individuals approaching retirement, health-conscious consumers, and budget-minded insurance shoppers, market-based reforms can be particularly appealing. They offer the potential for greater control over healthcare spending, more personalized options, and a reduced reliance on government programs. The focus on individual responsibility aligns with conservative values and offers a path towards a more sustainable healthcare system.

Key Features of Market-Based Reforms:

Expansion of Health Savings Accounts (HSAs) and tax deductions: HSAs allow individuals to save pre-tax dollars for qualified medical expenses, promoting personal responsibility and cost-consciousness.

Interstate insurance sales: By allowing insurers to sell plans across state lines, competition increases, potentially driving down premiums and offering more choices.

Price transparency requirements: Mandating that providers disclose the cost of services empowers consumers to make informed decisions and shop for the best value.

Reduced insurance mandates and regulations: Fewer mandates allow insurers to offer a wider variety of plans at different price points, catering to individual needs and preferences.

Association Health Plans (AHPs): These plans allow small businesses and self-employed individuals to band together to purchase insurance, increasing their bargaining power and potentially lowering costs.

High-risk pools for those with pre-existing conditions: These pools aim to provide coverage options for individuals who might otherwise be denied coverage in a more competitive market.

Pros:

Potential for innovation through market competition: A competitive market encourages insurers and providers to develop innovative solutions and improve the quality of care.

Consumer choice and flexibility: Individuals have more control over their healthcare decisions and can choose plans that align with their values and needs.

Reduced government intervention and costs: Less government involvement can lead to lower administrative costs and a more efficient healthcare system.

Encourages direct price competition among providers: Transparency and competition can drive down prices for medical services.

Could lower premiums for healthy individuals: With less stringent mandates, insurers can offer more affordable plans for those who are generally healthy.

Cons:

May leave vulnerable populations with inadequate coverage: Concerns exist that a purely market-based system may leave some individuals, particularly those with low incomes or pre-existing conditions, without access to affordable and comprehensive coverage.

Potentially higher costs for those with pre-existing conditions: High-risk pools, while intended to address this issue, have historically been underfunded and expensive.

Risk of "bare-bones" insurance plans that don't cover essential services: Competition could lead to plans that offer minimal coverage, leaving individuals exposed to significant financial risk in case of serious illness or injury.

May not address systemic healthcare inequality: Market-based reforms alone may not address underlying issues of access and affordability for disadvantaged populations.

Examples of Market-Based Reforms:

2017 Republican healthcare proposals: Several proposals aimed to repeal and replace the Affordable Care Act with market-based reforms.

Singapore's healthcare system: Combines public and private elements with medical savings accounts, offering a model of consumer-driven healthcare.

Switzerland's regulated private insurance market: All citizens are required to purchase insurance from private companies, with subsidies available for low-income individuals.

When and Why to Consider Market-Based Reforms:

If you prioritize choice, flexibility, and personal responsibility in healthcare and believe that a less regulated market can lead to better outcomes and lower costs, then market-based reforms might be a suitable alternative to Obamacare for you. This approach is particularly attractive to those who are generally healthy, comfortable navigating a more complex healthcare marketplace, and prefer to manage their own healthcare spending. However, it's crucial to carefully weigh the potential benefits and drawbacks, especially if you have pre-existing conditions or concerns about access to affordable care. This approach deserves its place on this list as a viable alternative for those who seek a free-market solution to healthcare.

4. State-Based Solutions: Tailoring Healthcare to Local Needs

As an alternative to Obamacare, state-based solutions propose shifting the power of healthcare decision-making away from the federal government and back to individual states. This approach argues that a one-size-fits-all healthcare system isn't effective for a nation as diverse as the United States. Instead, it empowers states to act as "laboratories of democracy," experimenting with different models and tailoring their healthcare systems to the specific needs and preferences of their residents. This devolution of power is often achieved through mechanisms like federal block grants and waivers, offering states greater flexibility in designing their coverage requirements and managing their healthcare budgets. For conservative American families, individuals approaching retirement, health-conscious consumers, budget-minded insurance shoppers, and patriotic individuals seeking more local control, this approach offers a potentially appealing alternative to the current system.

How State-Based Solutions Work:

The core principle behind state-based solutions is decentralization. Instead of a federally mandated system, states would receive block grants for healthcare funding. This fixed amount of federal funding would give states more autonomy over how they spend their healthcare dollars. States could then design their own benefit packages, set their own eligibility criteria, and negotiate directly with providers. Expanded Medicaid waiver authority further enhances state flexibility in administering this program. This localized approach aims to reduce federal bureaucracy, foster innovation, and address regional cost variations more effectively.

Features of State-Based Solutions:

Federal Block Grants: States receive a fixed sum of money for healthcare, allowing for more budgetary control.

Flexible Coverage Requirements: States define the essential health benefits that insurance plans must cover, potentially offering more customized options.

Expanded Medicaid Waivers: States gain more flexibility in how they administer their Medicaid programs.

Local Control: Healthcare policy decisions are made at the state level, closer to the people they affect.

Diverse Approaches: Different states can implement unique models, fostering innovation and competition.

Reduced Federal Mandates: Fewer federal regulations allow states to adapt their systems more readily to local needs.

Examples of State-Based Solutions in Action:

Several states have already explored elements of this approach, offering glimpses into its potential:

Massachusetts: The state's health reform under Governor Romney, which predated the ACA, served as a model for the federal law, although it maintained significant state control.

Vermont: The state pursued a single-payer healthcare system, demonstrating a state's ability to pursue innovative models. While ultimately unsuccessful, it highlighted the potential for experimentation under a state-based approach.

Section 1332 ACA Innovation Waivers: These waivers, part of the ACA itself, allow states to experiment with different healthcare models while maintaining certain core protections.

Oregon's Coordinated Care Organizations: These organizations integrate physical, mental, and dental health services at the local level, demonstrating how states can innovate within a broader framework.

Pros and Cons:

Pros:

Customization: Tailors healthcare to the specific needs and demographics of each state's population.

Innovation: Encourages experimentation and allows for successful models to be adopted by other states.

Cost Control: Potentially addresses regional cost variations more effectively than a national system.

Reduced Bureaucracy: Streamlines administration by shifting decision-making away from the federal government.

Cons:

Uneven Coverage: Could lead to disparities in coverage and benefits between states.

Vulnerable Populations: Raises concerns about potential reductions in protections for vulnerable populations.

Administrative Inefficiency: Managing 50 different systems could create administrative complexities.

Interstate Migration: Differences in coverage could incentivize migration based on healthcare access.

Block Grant Shortfalls: Fixed block grants might not adjust adequately for population growth or economic downturns.

When and Why to Consider State-Based Solutions:

This approach is particularly attractive to those who believe that healthcare decisions are best made at the local level. If you value state autonomy, desire more customized healthcare options, and believe in the power of local experimentation, then state-based solutions merit serious consideration as an alternative to Obamacare. This model is frequently championed by organizations such as the American Legislative Exchange Council (ALEC) and various State Policy Network organizations, reflecting its appeal to those seeking market-based healthcare reform. While it offers potential advantages, it is crucial to weigh the potential risks and consider the potential impact on access, affordability, and quality of care. This approach calls for careful consideration of how to balance state flexibility with the need to maintain essential protections for all Americans.

5. Universal Catastrophic Coverage: A Safety Net for Medical Disaster

For conservative American families, individuals approaching retirement, and budget-minded insurance shoppers seeking alternatives to Obamacare, Universal Catastrophic Coverage (UCC) presents a compelling option. This approach prioritizes financial protection from devastating medical expenses while promoting individual responsibility for routine healthcare costs. It offers a potential middle ground, appealing to those seeking a market-based approach with a strong safety net. This alternative to Obamacare aims to protect you from medical bankruptcy while fostering cost-conscious healthcare decisions.

What is Universal Catastrophic Coverage?

UCC establishes a government-backed insurance program covering exceptionally high medical costs for all Americans. Think of it as a safety net catching you before you fall into medical bankruptcy. Routine checkups, minor illnesses, and moderate medical expenses would be handled through individual payment, private insurance, or supplemental coverage. This structure encourages responsible spending for everyday healthcare needs while ensuring catastrophic events don't lead to financial ruin.

How Does it Work?

UCC operates on a two-tiered system. The first tier, the catastrophic coverage, is universally available and funded by the government. Importantly, deductibles are tied to income – higher for the wealthy, lower for those with limited resources. This ensures the system remains equitable and protects vulnerable populations. The second tier involves a vibrant private supplemental insurance market for routine care. Individuals can choose plans that best fit their needs and budget, fostering competition and innovation among insurers. This market-based approach empowers consumers to make informed decisions about their healthcare spending.

Features and Benefits:

Universal Protection: Every American is shielded from the financial devastation of major health crises, regardless of employment status or pre-existing conditions.

Income-Based Deductibles: A sliding scale for deductibles ensures fairness and affordability.

Market-Driven Routine Care: The private supplemental insurance market encourages competition and consumer choice, potentially lowering costs for routine procedures and services.

Simplified Administration: Compared to complex subsidy systems, UCC is potentially simpler to administer, reducing bureaucratic overhead.

Examples and Inspiration:

Elements of catastrophic coverage are successfully incorporated into Singapore's healthcare system, renowned for its efficiency and affordability. Closer to home, Medicare Part A (hospital insurance) shares some conceptual similarities with UCC. Economists like Martin Feldstein and Jonathan Gruber, the Niskanen Center, reform-minded policy experts, and health policy analyst Avik Roy have all contributed to popularizing this idea.

Pros and Cons:

Pros:

Protection from Medical Bankruptcy: Provides a crucial safety net for all Americans.

Potential Cost Savings: Encourages price sensitivity for routine care, potentially reducing overall healthcare spending.

Broad Appeal: Could find support across the political spectrum.

Market-Based Approach: Maintains market forces for most healthcare decisions.

Cons:

Preventive Care Disincentives: Individuals might postpone routine checkups and screenings to avoid costs, potentially leading to more serious health problems down the line.

Coverage Gaps: Moderate medical needs might still pose a financial burden.

Defining "Catastrophic": Establishing a clear definition of what constitutes a "catastrophic" event can be complex.

Systemic Inefficiencies: May not address underlying inefficiencies in the healthcare delivery system.

Political Hurdles: Implementing such a significant change could face political resistance.

Why Choose Universal Catastrophic Coverage?

If you're a patriotic individual seeking a fiscally responsible, market-based alternative to Obamacare, UCC warrants serious consideration. It balances individual responsibility with a critical safety net, ensuring that a major medical crisis doesn't derail your financial future. This approach acknowledges the importance of personal responsibility for routine health management while safeguarding against unforeseen and potentially devastating medical events. For those prioritizing financial security and peace of mind, Universal Catastrophic Coverage offers a compelling alternative to the complexities of the current healthcare system.

6. Multi-Payer Universal Coverage: A Blended Approach to Healthcare

For those seeking alternatives to Obamacare, multi-payer universal coverage presents a potential middle ground between a fully private system and a single-payer model. This approach aims to achieve universal health insurance coverage – meaning everyone has access – by leveraging a regulated mix of public and private insurers. It offers a potentially less disruptive transition from the current U.S. system, which is a key consideration for many, especially conservative American families and individuals approaching retirement.

How it Works:

Multi-payer universal coverage mandates health insurance for all citizens, similar to the individual mandate under the Affordable Care Act (often referred to as Obamacare). However, unlike a single-payer system where the government is the sole insurer, this model retains the role of private insurance companies. These private insurers operate within a regulated market with standardized benefits, ensuring a baseline level of care for everyone. The government plays a crucial role by providing income-based subsidies to help low-income individuals and families afford coverage, and by strongly regulating insurance providers to prevent abuses and ensure fair pricing. All-payer rate setting, a system where prices for medical services are negotiated and set across all insurers, is often a component to control provider costs. Additionally, a public option is often available for those who cannot access or afford private insurance, offering a safety net and promoting competition within the marketplace.

Real-World Examples:

Several countries successfully employ multi-payer universal coverage systems, demonstrating its viability. Germany's statutory health insurance system, Switzerland's regulated private insurance market, the Netherlands' managed competition model, and Japan's employment-based system with community rating all offer insights into different implementations of this approach. These nations consistently rank high in healthcare outcomes, suggesting that multi-payer systems can deliver quality care.

Why Consider Multi-Payer Universal Coverage?

This approach offers a blend of public oversight and private sector involvement, potentially appealing to budget-minded insurance shoppers and patriotic individuals who value market-based solutions. It strives to achieve universal coverage, addressing a core concern for health-conscious consumers, while maintaining consumer choice among insurance plans and potentially fostering competition to drive efficiency. This is a significant advantage over a single-payer system, which often limits choices.

Pros and Cons:

Pros:

Universal Coverage with Private Sector Involvement: This model offers a pathway to universal healthcare without completely eliminating the private insurance industry, a crucial consideration for many Americans.

Less Disruptive Transition: It builds upon the existing system, potentially easing the transition and minimizing upheaval.

Potential for Market Efficiency: Competition among private insurers can drive innovation and cost-effectiveness.

Consumer Choice: Individuals retain the ability to choose among different insurance plans.

Cons:

Complex Regulatory Framework: Effective regulation and oversight require a sophisticated and potentially complex bureaucratic structure.

Higher Administrative Costs: Compared to single-payer systems, multi-payer systems tend to have higher administrative costs due to the involvement of multiple insurers.

Government Oversight Challenges: Strong government oversight is crucial to prevent abuses and ensure fair pricing, which can be challenging to implement and enforce.

Potential for Regional Disparities: Even with regulation, regional disparities in access to care may persist.

Industry Opposition: Strong industry opposition to price controls and regulations is likely.

Actionable Tips:

If you are considering a multi-payer system as an alternative to Obamacare, research the examples of countries mentioned above. Compare their models and consider which aspects might best suit the American context. Pay close attention to how these systems address issues of cost control, consumer choice, and access to care.

When and Why to Use This Approach:

This approach is best suited for those who believe in the power of market forces but also recognize the need for government intervention to ensure universal access and affordability. It offers a potential compromise for those who are wary of a complete government takeover of healthcare but also dissatisfied with the current system. For conservative American families and others seeking a balanced approach, multi-payer universal coverage deserves serious consideration as an alternative to Obamacare.

7. Healthcare Delivery Reform: Fixing the System, Not Just the Insurance

Healthcare Delivery Reform offers a different perspective on alternatives to Obamacare. Instead of solely focusing on who pays for healthcare (insurance), it tackles how healthcare is delivered and paid for. This approach aims to improve the value and efficiency of the system itself, making healthcare more affordable and effective for everyone, regardless of their insurance plan. This makes it a compelling option for conservative American families, individuals approaching retirement, health-conscious consumers, budget-minded insurance shoppers, and anyone seeking a more sustainable healthcare system.

This method works by shifting away from the traditional fee-for-service model, where providers are paid for each procedure or visit, regardless of the outcome. Instead, it emphasizes value-based care, rewarding providers for keeping patients healthy and achieving better outcomes. This aligns incentives with quality and efficiency.

Key Features of Healthcare Delivery Reform:

Value-based payment models: Replacing fee-for-service with payments based on quality metrics and patient outcomes.

Accountable Care Organizations (ACOs): Networks of doctors, hospitals, and other healthcare providers who work together to provide coordinated care.

Patient-Centered Medical Homes: A model of primary care that emphasizes comprehensive, coordinated care focused on the patient's needs.

Bundled payments for episodes of care: A single payment covering all services related to a specific health issue or condition.

Price transparency initiatives: Making healthcare costs more transparent for consumers.

Telehealth expansion: Expanding access to care through virtual visits and remote monitoring.

Focus on preventive care and chronic disease management: Keeping people healthy and managing chronic conditions effectively to reduce long-term costs.

Pros:

Works within multiple insurance frameworks: Delivery reform can be implemented within both private and public insurance systems, making it a flexible alternative to Obamacare.

Addresses root causes of healthcare cost growth: By focusing on efficiency and value, it tackles the underlying drivers of rising healthcare costs.

Potential to improve patient outcomes and experiences: Coordinated, patient-centered care can lead to better health outcomes and a more positive patient experience.

Bipartisan support: Many delivery reforms enjoy bipartisan support, increasing the likelihood of successful implementation.

Evidence-based approach using quality metrics: Data and evidence are used to track progress and ensure that reforms are effective.

Cons:

Doesn't directly address insurance coverage gaps: While it can lower costs, it doesn't directly address the issue of uninsured individuals. However, by making the system more efficient, it can free up resources to expand coverage options.

Complex to implement across a fragmented healthcare system: Implementing these changes requires significant coordination and collaboration across different parts of the healthcare system.

Requires significant provider buy-in and system changes: Providers need to adapt to new payment models and ways of working.

Benefits may take years to fully realize: Transforming a complex system like healthcare takes time, and the full benefits may not be seen immediately.

May require substantial initial investment: Investing in new technologies and infrastructure can be costly upfront.

Examples of Successful Implementation:

Medicare's various Alternative Payment Models: Medicare has been experimenting with various value-based payment models, with some showing promising results.

Blue Cross Blue Shield's patient-centered medical home initiatives: These initiatives have demonstrated improved patient outcomes and cost savings.

Kaiser Permanente's integrated care delivery model: Kaiser's integrated system is often cited as a model for coordinated care.

Maryland's all-payer global budget system: Maryland's unique system sets a global budget for hospital spending, incentivizing hospitals to control costs and improve efficiency.

Actionable Tips:

Research and compare different providers: Look for providers who are participating in value-based care programs.

Ask your doctor about care coordination: Inquire about how your care is coordinated across different providers.

Utilize telehealth options: Explore telehealth options for routine appointments and follow-up care.

Focus on preventive care: Prioritize preventive care and healthy lifestyle choices.

When and Why to Use This Approach:

Healthcare Delivery Reform is a valuable alternative to Obamacare for those who believe the system itself needs to be reformed, not just the insurance market. This approach is particularly appealing to those who prioritize long-term sustainability, value, and efficiency in healthcare.

Healthcare Delivery Reform deserves its place on this list because it provides a fundamental shift in how we approach healthcare. This isn't just about finding a cheaper insurance plan; it's about building a better, more sustainable system for the future. Popularized by organizations like the Institute for Healthcare Improvement and the Center for Medicare and Medicaid Innovation (CMMI), and championed by thought leaders such as Dr. Donald Berwick and Dr. Atul Gawande, this approach focuses on getting the most value out of every healthcare dollar spent.

7 Alternatives to Obamacare Comparison

Plan | 🔄 Implementation Complexity | 💡 Resource Requirements | 📊 Expected Outcomes | ⭐ Key Advantages | 💡 Ideal Use Cases |

|---|---|---|---|---|---|

Medicare for All | High – Single-payer overhaul with major system disruption | Very high – Requires substantial tax increases and admin reorg | Universal coverage; reduced out-of-pocket costs; possible wait times | Universal coverage; simplified financing; cost negotiation | Nationwide universal healthcare with equity goals |

Public Option | Medium – Adds government plan alongside private insurers | Moderate – Requires system integration and negotiation efforts | Increased competition; potential premium reduction; incomplete coverage | Less disruptive; competitive pricing; politically feasible | State or national additions to existing multi-payer systems |

Market-Based Reforms | Medium – Regulatory rollbacks and market incentives | Moderate – Depends on tax incentives and regulatory changes | Increased competition; consumer choice; risk of coverage gaps | Promotes innovation; consumer flexibility; reduced gov. role | Enhancing free-market mechanisms in healthcare |

State-Based Solutions | Medium-High – Federal-to-state authority transition | Moderate to high – State-level policymaking and admin capacity | Variable coverage; policy innovation; risk of disparities | Regional customization; policy experimentation | States with distinct healthcare needs or reform ambitions |

Universal Catastrophic Cov | Medium – Focus on high-cost coverage with private supplementation | Moderate – Funding catastrophic coverage with income-based deductibles | Financial protection against major expenses; cost-conscious care | Protects from bankruptcies; encourages routine care cost awareness | Systems seeking to limit catastrophic financial risk |

Multi-Payer Universal Cov | High – Complex regulation and enforcement | High – Subsidies, regulation, and rate setting required | Universal coverage with private insurers; administrative overhead | Maintains choice; tested in many countries | Mixed public-private universal coverage frameworks |

Healthcare Delivery Reform | Medium-High – System-wide payment and care delivery changes | High – Requires provider cooperation and investments | Improved outcomes; cost control; long realization timeline | Addresses cost drivers; bipartisan support; value focus | Improving quality and efficiency within existing insurance |

Choosing the Right Path: Your Healthcare Journey

Navigating the complex landscape of healthcare can feel overwhelming. This article has explored several key alternatives to Obamacare, ranging from systemic overhauls like Medicare for All and a Public Option to market-based reforms, state-driven solutions, and innovative approaches like Universal Catastrophic Coverage. We've also touched on the importance of healthcare delivery reform and the potential of multi-payer universal coverage. Understanding these alternatives empowers you to make informed decisions about your health and financial well-being, a critical step in securing a healthier future for yourself and your family. The most important takeaway is that there are options available, and finding the right fit for your unique situation is achievable.

Mastering these concepts allows you to engage in productive conversations about healthcare policy, advocate for solutions aligned with your values, and ultimately, choose a path that empowers you. Whether you prioritize individual liberty, cost-effectiveness, comprehensive coverage, or a combination of factors, the goal is to find an approach that supports your health and financial goals. The right approach allows you to take control of your healthcare journey and build a more secure future.

For those seeking alternatives to Obamacare grounded in conservative principles and focused on affordability and family-centric care, explore the options available at America First Financial. We offer a range of healthcare plans designed to meet the diverse needs of American families and individuals. Visit America First Financial today to learn more and discover how we can help you secure a healthier future.

Comments