_edited.png)

Top Long Term Care Insurance Providers You Can Trust

- dustinjohnson5

- Aug 24, 2025

- 13 min read

Long-term care insurance is one of those financial tools that's easy to put off, but it’s absolutely essential for protecting your family’s future. Think of it as a dedicated safety net for the costs of daily living assistance, whether that’s at home or in a facility. This isn't something covered by your regular health plan, and that’s a distinction that matters. Finding the right provider is how you safeguard your assets and give your family real peace of mind.

Why Planning for Long Term Care Is Essential

It’s a common—and dangerous—misconception that health insurance or Medicare will step in to cover extended care. In reality, those programs are built for short-term, acute medical events, like a hospital visit after a fall, not the long-term custodial care that many of us will eventually need.

Custodial care is the non-medical, hands-on help with daily life—things like getting dressed, bathing, or preparing meals. Without a dedicated long-term care policy, those costs come straight from your retirement nest egg, and they can be staggering, often climbing into the six figures each year.

Understanding the Coverage Gap

To really see why a long-term care policy is so crucial, you have to look at what other insurance plans don't cover. There's a massive gap right where families need the most help: ongoing, non-medical support.

Long Term Care Insurance vs Other Coverage

This simple breakdown shows just how different these policies are. Notice where the "No"s start to pile up for traditional plans.

Coverage Type | Covers In-Home Skilled Nursing | Covers Assisted Living Costs | Covers Custodial Care (Non-Medical) | Covers Chronic Conditions |

|---|---|---|---|---|

Long Term Care Insurance | Yes | Yes | Yes | Yes |

Traditional Health Insurance | Limited/Short-Term Only | No | No | Limited |

Medicare | Limited/Post-Hospital Only | No | No | Limited |

As you can see, only long-term care insurance is designed from the ground up to handle these specific, long-duration needs. It’s no surprise the global market for this type of insurance was recently valued at around USD 80 billion and continues to grow as more people recognize the need to plan ahead.

A Real World Financial Scenario

Let’s put this into perspective. A client of mine, a retired engineer, had a stroke. He recovered, but he could no longer manage things on his own at home.

His health insurance was great for the hospital stay and the initial rehab, but that's where the coverage stopped. Once he was back home, the family was on the hook for daily help. They were looking at a tough decision: either drain their savings to pay thousands a month for professional care or have one of their adult children quit a job to become a full-time caregiver.

A long-term care policy would have changed everything. It would have covered a professional in-home caregiver, preserving the family's finances and, just as importantly, their emotional well-being.

A well-structured LTCI policy is not just about paying bills; it’s about providing options, dignity, and control when your family needs it most. It safeguards the legacy you've worked a lifetime to build.

Thinking about how this fits into your overall financial strategy is smart. For a broader view, looking into resources on Arkansas Estate Planning can help you see how all the pieces come together to secure your family's future.

How to Evaluate Top Insurance Providers

Choosing a long-term care insurance provider is one of the most important financial decisions you’ll make. This isn't just about buying a policy; it's about finding a reliable partner you can count on, possibly decades from now when you're most vulnerable. You need to look past the slick marketing and really dig into the company's stability and character.

This is more critical today than ever before. Back in the 90s, over 100 companies were in this market. Now, fewer than 15 are still writing new policies. Even so, the industry expects to pay out a staggering $42 billion in claims around 2041. You can read more about these long-term care industry projections on milliman.com. This tells you one thing loud and clear: you have to pick a company built to last.

Assess Financial Stability and Ratings

First things first: a policy is worthless if the company behind it can't pay the bills. You need to be sure the insurer you choose is on solid financial ground and will still be standing strong when it's time to file a claim.

The best way to do this is to check their scores from independent rating agencies. Think of these as financial report cards.

[A.M. Best](https://www.ambest.com/): Anything less than an A+ or A++ ("Superior") should give you pause.

[Moody's](https://www.moodys.com/): Look for Aa or A ratings, which signal strong creditworthiness.

[Standard & Poor's (S&P)](https://www.spglobal.com/ratings/en/): Stick with companies rated AA or A for "Very Strong" to "Strong" financial security.

These aren't just arbitrary letters. They reflect a deep dive into a company's cash reserves, investment strategies, and overall financial discipline.

I’ve seen what happens when people ignore this. After the 2008 financial crisis, some folks with policies from lower-rated insurers were hit with massive, unexpected premium increases. In the worst cases, their provider went under. State guarantee funds can help, but it’s a headache you don’t need. It’s always better to start with a rock-solid company.

Evaluate Claims Payment History

A company can have a mountain of cash, but if they fight you tooth and nail on every claim, what good is it? You need an insurer with a proven track record of paying valid claims fairly and without unnecessary delays.

So, how do you find out? Start by checking with your state's department of insurance for consumer complaint data. You can also search for online reviews, but take them with a grain of salt. A few grumpy customers are normal for any business. What you're looking for is a consistent pattern of problems—that’s a serious red flag.

Scrutinize Customer Service and Support

When the time comes to use this policy, you won't be talking to the CEO. You'll be dealing with customer service reps, and their competence and compassion can make all the difference during a stressful time.

Here’s a practical tip: before you sign anything, give their customer service line a call. Ask a few basic questions about their claims process or a policy feature. This simple test can tell you a lot about their company culture. If they’re helpful and easy to deal with now, chances are they'll be there for you when it really counts.

Choosing Between Traditional and Hybrid LTC Policies

When you start looking into long-term care insurance, you’ll quickly find yourself at a fork in the road. On one side, you have traditional, standalone LTC policies. On the other, you have modern hybrid policies that combine life insurance with long-term care benefits. There’s no single “best” answer here; the right path really depends on your family's financial philosophy and what you’re trying to accomplish.

Let's walk through this with a couple of real-world scenarios. Imagine the Martins, a couple focused purely on getting the most care coverage for every dollar they spend. Then think about the Jacksons, who want more flexibility and a guarantee that their money won't be lost if they never end up needing care.

The Traditional Policy Approach

The Martins, both in their late 50s, decided to go with a traditional policy. Their number one priority is protecting their hard-earned assets from the staggering costs of long-term care. A traditional plan gives them the biggest bucket of money specifically for care, maximizing the potential benefit for their premiums.

The concept is simple: you pay premiums for a dedicated LTC benefit. If you need care, the policy pays. If you pass away without needing care, the policy ends, and there's no payout. The Martins were okay with this “use it or lose it” model because their primary fear was a catastrophic care event wiping out their savings.

They were, however, mindful of one of the drawbacks of traditional plans: premiums aren't always guaranteed. To counter this, they were very selective and chose one of the best long term care insurance providers known for a long history of stable rates, mitigating that risk as much as possible.

The Hybrid Policy Advantage

The Jacksons, a bit younger, approached this differently. They just couldn't stomach the thought of paying into a policy for decades that they might never use. So, they opted for a hybrid life insurance policy that comes with a long-term care rider. This setup provides a single, guaranteed premium that will never go up.

Here’s how their policy is structured:

If they need long-term care: They can tap into a large portion of the life insurance death benefit while they're still alive to cover their care costs.

If they never need long-term care: Their children will receive the full, tax-free death benefit when they pass away.

If they only use a portion of the care benefits: Their children get whatever is left of the death benefit.

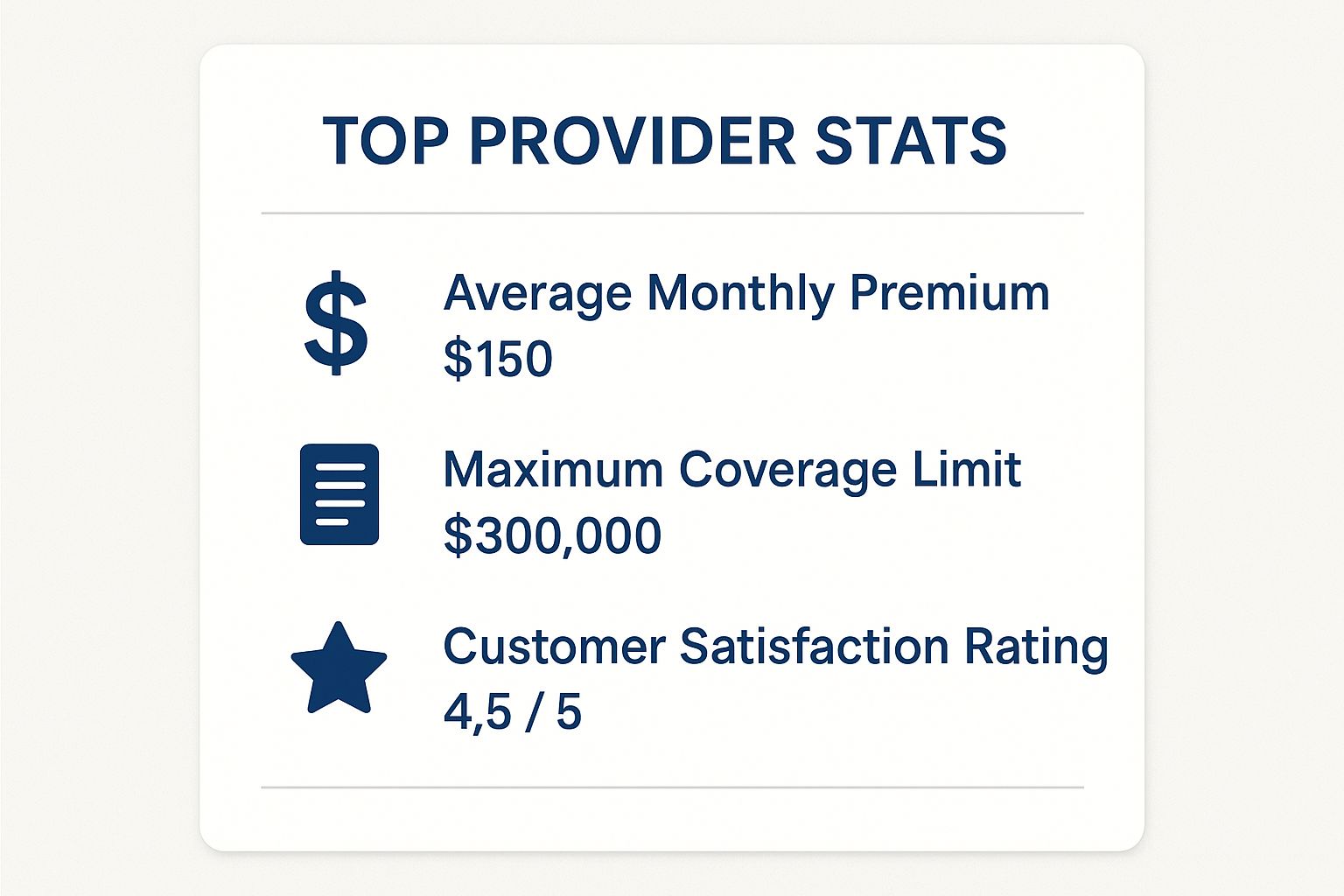

This chart breaks down some of the key statistics you'll want to weigh when you compare different insurance carriers.

As you can see, there's a constant balancing act between the monthly cost, the total coverage you get, and the insurer's reputation for service.

A hybrid policy completely sidesteps the "use it or lose it" problem. It gives you the comfort of knowing that, one way or another, your family will see a return on the premiums you paid.

For the Jacksons, that built-in guarantee was the deciding factor. Even though their potential LTC benefit might be a little less than what a comparable traditional plan would offer, the locked-in premium and the certainty of a payout aligned perfectly with their conservative financial goals.

Traditional vs Hybrid LTC Insurance Policies

To help you see the differences side-by-side, here’s a quick comparison. Think about your own priorities as you review it—are you aiming for maximum leverage or maximum flexibility?

Feature | Traditional LTC Insurance | Hybrid (Life + LTC) Insurance |

|---|---|---|

Primary Goal | Maximizes LTC benefits for the premium paid. Pure protection. | Provides a death benefit and LTC coverage. Dual-purpose. |

Premiums | Can potentially increase over time. Not always guaranteed. | Typically a single, guaranteed premium that will never increase. |

"Use It or Lose It" | Yes. If you don't need care, there is no payout or return of premium. | No. If you don't need care, your heirs receive a life insurance death benefit. |

Underwriting | Health underwriting can be strict, focused on long-term health risks. | Often simpler health underwriting as part of a life insurance application. |

Best For | Families whose primary goal is to get the most LTC coverage for their dollar. | Families who want a guaranteed return on their premium and hate the idea of "wasting" money. |

Ultimately, the choice between traditional and hybrid LTC insurance comes down to your personal risk tolerance and financial strategy. By understanding these core differences, you can make a much more informed decision that truly fits your family’s needs.

Customizing Your Policy for Maximum Value

Picking a top-rated long-term care insurance provider is a great first step, but it's only half the journey. Now comes the critical part: tailoring that policy to fit your family’s unique situation and, just as importantly, your budget.

Think of it this way: a standard policy is like a model home. It has a great foundation, but the real value comes when you choose the finishes that make it your home. With long-term care insurance, you get to adjust the key components—the dials and levers—that control both your future benefits and what you pay today. This is where you can build a smart, efficient plan that truly protects your assets.

Adjusting Your Daily Benefit Amount

The daily benefit amount is exactly what it sounds like: the maximum amount the policy will pay for your care each day. This is one of the biggest factors influencing your premium. A higher daily benefit offers a bigger safety net, but it will cost you more upfront.

So, how do you find the right number? Start by researching the cost of care where you live. If a local nursing home runs $300 a day, a policy with a $200 daily benefit means you'll be covering a $100 shortfall out-of-pocket. But if your plan is to receive care at home—which is often the preference and can be less expensive—that $200 daily benefit might be more than enough. The goal isn't to cover every last penny, but to cover a substantial portion of the likely cost without paying for more insurance than you need.

Setting the Benefit Period

Next up is the benefit period, which is simply how long your policy will pay out once you begin to need care. You'll typically see this expressed in years—two, three, five, or sometimes even for life. This, combined with your daily benefit, determines your total pool of money.

Let’s run the numbers. A policy with a $200 daily benefit and a three-year period gives you a total benefit pool of about $219,000. Bump that up to a five-year period, and your total pool grows to $365,000. Naturally, the longer period costs more. In my experience, many families find that a benefit period in the three-to-five-year range hits the sweet spot between robust protection and a manageable premium.

The Power of Inflation Protection

This might be the single most important decision you make when designing your policy. A dollar today won't buy a dollar's worth of care in 20 years. That's a fact. An inflation rider is what makes sure your benefits keep up with rising costs.

You generally have a couple of choices here:

Simple Inflation: This increases your benefit by a set percentage of your original benefit amount each year. It’s predictable but less powerful.

Compound Inflation: This is the one to pay attention to. Your benefit increases based on the previous year's total, creating a snowball effect over time.

A 5% compound inflation rider can easily double your benefit pool in about 15 years. Yes, it adds to the premium, but without it, you risk your policy's purchasing power eroding to the point where it offers little real protection when you need it most.

If you're trying to decide where to allocate your premium dollars, my advice is to prioritize a strong inflation rider. A slightly smaller daily benefit that grows significantly over time is almost always a smarter move than a large, flat benefit that gets eaten away by inflation.

By carefully considering these three elements, you can move beyond a generic plan and design a policy that truly reflects your family’s conservative financial principles. It’s not about buying the biggest policy available; it’s about buying the smartest one for your future.

Navigating the Application and Underwriting Process

Once you've zeroed in on the right long-term care insurance provider, the next step is underwriting. It sounds a bit clinical, but all it really means is that the insurance company needs to get a clear picture of your health before they offer you a policy.

Think of it as a comprehensive health review. They'll look over your medical records, have you fill out a health questionnaire, and usually conduct a brief phone interview. The goal is simple: to understand your health history and current condition. Being organized and upfront here will make the entire experience go much more smoothly.

Preparing for a Smooth Application

You can save yourself a lot of headaches by gathering all your information before you even start the application. A little prep work goes a long way in speeding up the approval and avoiding frustrating delays.

Here’s a practical checklist to get you started:

Your Doctors: Make a list of every doctor you've seen in the past 5 to 10 years, complete with their names and contact info.

Your Medications: Jot down every prescription you currently take, including the dosage and why you're taking it.

Your Health History: Be prepared to talk about any past surgeries, chronic illnesses, or significant health events in your family.

Having this information ready not only makes the process faster but also shows the underwriter you’re serious and organized. And I can't stress this enough: be completely honest. Trying to hide a pre-existing condition is one of the fastest ways to get your application denied or, even worse, have a claim denied down the road when you need it most.

The underwriting process is fundamentally about timing. Your health today is the single most important factor. Procrastination doesn't just cost more in premiums—it can cost you the ability to get coverage at all.

Why Acting While Healthy Is Critical

Let me share a common scenario that I’ve seen play out too many times. Take a couple, John and Mary, both 58, who decide it’s finally time to apply. Mary is in great health with no major issues, so she breezes through underwriting and gets her policy approved in a few weeks.

John, on the other hand, just saw his doctor about some nagging joint pain and was diagnosed with early-stage rheumatoid arthritis. While it's manageable, that new diagnosis is a major red flag for the insurance company. His application is ultimately denied.

This is a tough but crucial lesson: your health is your greatest asset when applying for this coverage. The reality is, demand for long-term care is growing, and projections show that spending in the U.S. could triple as a percentage of GDP by 2050. You can read more about the growing demand for long-term care on ajg.com.

John and Mary’s story shows how waiting even a few months can completely change the outcome, leaving one person without this vital protection for good. The best time to lock in your policy is when you’re healthy and feel like you don’t need it.

Your Top Long-Term Care Insurance Questions, Answered

Once you've dug into the strategies for picking a provider and designing a policy, a few practical questions almost always pop up. It's completely normal. Let's tackle some of the most common ones we hear from families just like yours.

What's the Best Age to Get Long-Term Care Insurance?

I get this question all the time. From my experience, the sweet spot for most people is their mid-50s. Applying at this age usually gets you more reasonable premiums and, just as importantly, you have a much better chance of sailing through the health underwriting.

If you put it off until you're in your late 60s or older, you’ll see the costs climb pretty steeply. But the bigger risk is a new health issue cropping up that could get you declined for coverage altogether. That risk goes up with every birthday.

Can I Deduct My Premiums on My Taxes?

You absolutely might be able to. Part of what you pay in premiums can often be counted as a medical expense when you're filing your taxes, but it hinges on your age and whether you itemize your deductions.

The IRS has set limits on how much you can deduct, and those limits get more generous as you age.

This is one of those areas where you really want to loop in your tax advisor. They can look at your specific financial picture and make sure you're taking full advantage of any tax breaks available to you.

What Happens If the Insurance Company Hikes My Rates?

Rate increases are a real possibility with older, traditional LTC policies—it’s something you have to be prepared for. If your provider does decide to raise rates, the law says they have to give you choices.

Usually, your options look something like this:

You can pay the higher premium to keep your benefits exactly as they are.

You can choose to reduce some of your benefits (like the daily payout amount) to keep your payment the same.

Sometimes, there's a "non-forfeiture" option that gives you a smaller, paid-up policy based on what you've already paid in.

This uncertainty is a major reason why so many families with a conservative mindset are now choosing hybrid policies. These almost always come with guaranteed premiums that are locked in for life, so you never have to worry about a surprise increase down the road.

Will My Coverage Still Work If I Move to a Different State?

For the most part, yes. Nearly all comprehensive long-term care policies sold these days are designed to be portable. That means your benefits travel with you, no matter where you decide to live in the United States.

Still, you need to confirm this before you sign anything. It's a critical detail. Make a point to ask the agent directly about any geographic limitations, especially if you're thinking about retiring out of state.

At America First Financial, we help you find long term care insurance that protects your family’s legacy without compromising your values. Get a straightforward, no-obligation quote in just a few minutes. Secure your future by visiting https://www.americafirstfinancial.org today.

Comments