_edited.png)

what is decreasing term life insurance: A quick guide

- dustinjohnson5

- Oct 31, 2025

- 12 min read

Imagine you've just taken on a big financial commitment, like a mortgage. It's exciting, but it's also a heavy weight. Decreasing term life insurance is like a specialized safety net built specifically for that weight, and it gets lighter as your burden does.

The policy starts with a death benefit big enough to cover the entire loan. Then, as you chip away at that mortgage year after year, the policy's coverage amount shrinks right alongside it. This way, your family is protected from that specific debt if you were to pass away unexpectedly, without being over-insured.

What Exactly Is Decreasing Term Life Insurance?

At its core, decreasing term life insurance is a type of temporary life insurance where the death benefit—the amount your family would receive—goes down over the life of the policy. This usually happens on a set schedule, often annually.

It’s built for one main job: to mirror the declining balance of a large loan.

Let's use a real-world example. Say you just bought a home with a $400,000 mortgage. Your financial responsibility is at its absolute highest. A decreasing term policy would kick off with a matching $400,000 death benefit. Fast forward fifteen years. You've been making payments, and your mortgage balance is now down to $220,000. The policy’s death benefit will have also dropped to roughly that same amount. This alignment is key—it ensures you're only paying for the coverage you actually need at any given time.

The Defining Features

Before diving deep into this specific product, it’s always a good idea to step back and ask the big question: when does life insurance make sense in the first place? For a broader look at that, this guide on Is Life Insurance Worth It? offers some great perspective.

With that context, here are the key traits that make decreasing term life insurance unique:

Shrinking Death Benefit: The payout your beneficiaries would get gets smaller over time.

Steady Premiums: Your payments usually stay the same for the entire term, so there are no surprises.

Targeted Purpose: It’s almost always tied to a loan that you're paying down, like a mortgage or a small business loan.

Lower Cost: Since the insurance company's potential payout (their risk) decreases every year, the premiums are typically cheaper than a comparable level term policy.

This structure offers a really smart, cost-effective way to protect your family's biggest asset—your home—without locking you into a large, fixed payout for decades.

For a quick overview, this table breaks down the essentials.

Decreasing Term Life Insurance at a Glance

Feature | Description |

|---|---|

Primary Goal | To pay off the remaining balance of a specific large debt, most commonly a mortgage. |

Death Benefit | Starts high to match the initial loan amount and decreases over the policy term. |

Premium Cost | Generally lower than level term insurance for the same initial coverage amount. |

Best For | Families or individuals seeking an affordable way to ensure a major loan is covered. |

Think of it as pure, no-frills protection designed for a very specific, and very common, financial need.

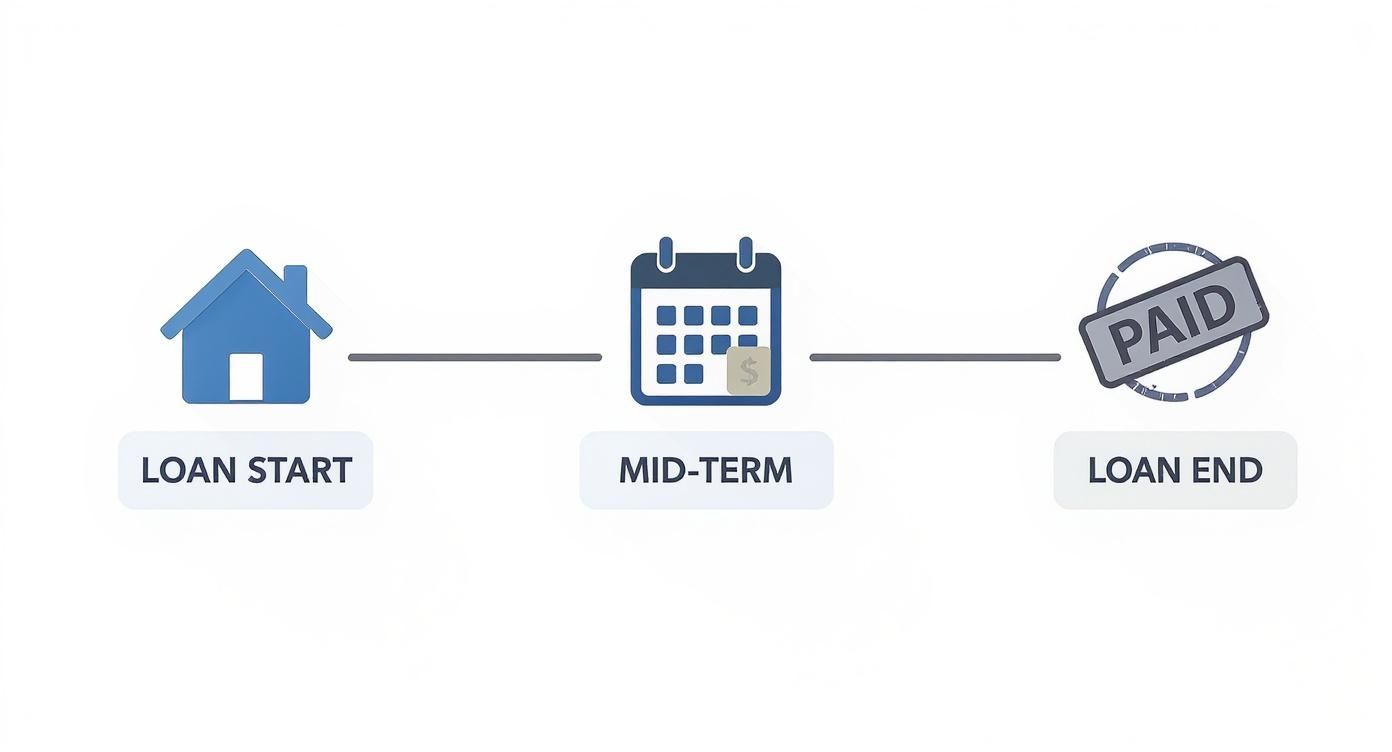

How Decreasing Term Coverage Actually Works

To really get a feel for how decreasing term life insurance works, think of it as a financial safety net designed to shrink right alongside a specific debt. Its whole purpose is to provide just enough money to pay off a loan—like a mortgage or a business loan—at any given time. No more, no less.

Let’s look at a classic example for a young American family: buying their first home. Say a couple takes out a 30-year mortgage for $300,000. Their biggest fear is that if one of them were to pass away, the other might lose the house. So, they buy a 30-year decreasing term policy with an initial death benefit of $300,000, matching their new mortgage perfectly.

Now, here’s a key detail that trips some people up: while the death benefit goes down every year, the premium payment typically remains level. This is actually a huge plus for family budgeting. You know exactly what you'll pay each month for the entire 30-year term, with no surprise rate hikes down the line.

A Mortgage Protection Timeline

To see this in action, let's track our couple’s policy over the years.

Year 1: If one of them were to pass away right after they moved in, the death benefit would be the full $300,000 (or very close to it). This would be enough to wipe out the mortgage, securing the home for the surviving family members.

Year 15: They're now halfway through their loan. Thanks to 15 years of steady payments, their mortgage balance has dropped to around $185,000. The life insurance policy’s death benefit has also decreased to track that new, lower balance.

Year 25: With the finish line in sight, the mortgage is down to just $70,000. The policy's payout has also shrunk to match, still providing the exact amount needed to clear the remaining debt.

This timeline gives you a great visual of how the coverage amount is meant to follow a typical mortgage amortization schedule.

As you can see, the insurance coverage starts high and then tapers off, hitting zero right as the last mortgage payment is made.

The core idea here is efficiency. You aren't paying for a massive death benefit in the later years when your debt is much smaller.

The decline is all scheduled in advance, making sure your protection is always right-sized for your needs. It's a smart, disciplined way to protect your family's biggest asset without overpaying for coverage you no longer need. When the 30 years are up, both the mortgage and the policy simply end, having done their job perfectly.

Decreasing Term Versus Level Term Insurance

When you’re looking to protect your family’s future, the first step is always understanding the tools at your disposal. For most people, that means choosing between the two most common types of term life insurance: decreasing term and level term. They might sound similar, but they're built for entirely different jobs.

Here’s a simple way to think about it. Decreasing term is like a specialized wrench, perfectly sized to fit one specific bolt—like your mortgage. On the other hand, level term is more like a versatile, all-purpose adjustable wrench that can tackle a wide range of financial needs, from replacing your income to making sure your kids can go to college.

The Core Difference in Death Benefit

The biggest distinction between these two policies is the death benefit, which is the amount of money your family receives.

With a level term policy, that number stays put. If you get a $500,000 policy for a 20-year term, the payout is always $500,000, whether something happens in year one or year nineteen. It’s designed to provide a steady, predictable safety net.

A decreasing term policy is different. Its death benefit shrinks over time, usually on a set schedule. It’s built to mirror the declining balance of a big loan, making sure the payout is just enough to cover what you still owe. This targeted design is what sets it apart.

The choice between them really boils down to one simple question: Are you trying to cover a specific, shrinking debt, or are you trying to protect your family’s overall lifestyle and financial future?

How Premiums and Purpose Compare

Now, you might assume that since the death benefit on a decreasing term policy goes down, your premiums would, too. But that’s usually not the case—the premiums typically stay the same for the whole term.

So why would anyone choose it? Because the overall cost is lower. Since the insurance company’s potential payout gets smaller every year, their risk drops, too. This means premiums for decreasing term policies are often 15% to 25% lower than what you'd pay for a level term policy with the same starting coverage.

That affordability is exactly why it’s so popular for mortgage protection. While decreasing term is less common in the United States than level term, it's still a solid option, especially for homeowners. It’s worth remembering that term life insurance as a whole accounts for over 60% of all new individual life insurance policies sold, which shows just how much American families rely on temporary coverage. If you're interested in the details, you can explore more about U.S. life insurance market trends for a broader perspective.

To make things even clearer, let's put these two policy types side-by-side.

Comparing Decreasing Term and Level Term Insurance

The table below breaks down the key features of each policy to help you see which one might be a better fit for your family's needs.

Feature | Decreasing Term Life Insurance | Level Term Life Insurance |

|---|---|---|

Death Benefit | Shrinks over the policy's term, typically following a pre-set annual schedule. | Stays the same from the first day of the policy right through to the last day. |

Typical Premium | Costs less because the insurer's risk gets smaller over the life of the policy. | Costs more because the full death benefit is available for the entire term. |

Primary Purpose | To cover a specific, large debt that you're paying down, like a mortgage or a business loan. | To provide broad financial protection for needs like income replacement, college funding, or final expenses. |

Ultimately, one isn't "better" than the other—they just have different goals. The right choice depends entirely on what financial obligation you’re trying to protect.

Weighing the Pros and Cons

Like any financial product, decreasing term life insurance isn't a silver bullet. It's a specialized tool, and figuring out if it’s right for your family means taking an honest look at both its strengths and its weaknesses.

The big draw here is plain and simple: it costs less. The insurance company’s risk goes down every year right alongside your mortgage balance. Because their potential payout shrinks, they pass those savings on to you in the form of lower premiums. This often makes it the most affordable way to make sure your home is protected.

That lower cost also makes it an incredibly efficient way to cover one specific thing: a big, shrinking debt. You’re not paying for a giant death benefit you might not need 20 years from now. You're buying just enough coverage to do one job—pay off the house—and that's it.

The Upside: What It Does Best

The main advantages really come down to its focused, no-frills design.

Lower Premiums: Put a decreasing term policy next to a level term policy with the same starting death benefit, and the decreasing one will almost always be cheaper. That’s more money in your pocket each month for savings, investments, or just life.

Perfectly Matched Debt Protection: The policy is built to follow your loan’s payment schedule. As you pay down your mortgage, the coverage drops with it. This means you’re never over-insured or paying for coverage you don’t actually need.

Peace of Mind for Your Home: This is its bread and butter. It offers a straightforward promise: if something happens to you, your family gets to keep the house. For many, that's a priceless guarantee.

Think of it as a perfectly matched puzzle piece for your mortgage. It fits exactly where it needs to, providing efficient protection without waste.

The Downside: Where It Falls Short

Of course, the very thing that makes this policy so efficient is also its biggest drawback.

The most obvious downside is its declining value. While it’s great for a loan that’s getting smaller, it becomes less and less helpful for other things your family might need money for, like replacing your income or paying for college. A small payout 25 years down the road won't do much to cover those kinds of ongoing expenses.

This brings us to its other major weakness: it’s inflexible. Life rarely goes according to a 30-year plan. What if you refinance your home and extend the loan? Or take on a new business debt? Or have another child and your financial needs grow? A decreasing term policy is stuck on its original path and can't adapt, which could leave your family seriously underinsured if your life changes.

When Is This Policy the Right Choice?

So, when does a decreasing term policy actually make sense for a family's financial plan? This isn't a one-size-fits-all solution. It's a specialized tool that really shines when your main goal is to cover a large debt that gets smaller over time.

The classic, and by far the most common, reason to get this policy is to protect a mortgage. Picture a family buying their first home—it's exciting, but it also comes with their biggest debt ever. Their number one worry is often what would happen if one of them passed away. Could the other person afford to keep the house? A decreasing term policy is designed to track that shrinking mortgage balance, giving them an affordable and perfectly matched safety net.

This idea has been around for a while. Decreasing term life insurance actually gained a lot of traction in places like the UK back in the 1950s and 60s, when 25-year mortgages became the norm. The policy was built from the ground up to ensure the payout would always be just enough to cover whatever was left on the home loan. If you're curious about the history, you can find more on global insurance trends on swissre.com.

Key Scenarios for Decreasing Term

While paying off the house is the number one reason people buy this policy, it works just as well for other kinds of loans that shrink over a set schedule.

Covering Business Loans: An entrepreneur who takes out a big loan to grow their business can use this policy to make sure their family or business partners aren't left holding the bag. As the loan gets paid down, the coverage drops right along with it.

Securing Private Student Loans: Sometimes a parent co-signs a large private student loan for their child. A decreasing term policy can shield the parent's estate from being on the hook for the remaining balance if something happens to the student.

Paying Off Other Large Personal Loans: It’s also a smart way to cover other major debts with a clear end date, like a loan for an RV or a major home renovation project.

The common thread here is simple: a large, specific debt that gets smaller and smaller over a predictable timeline. Decreasing term life insurance acts as a financial backstop designed just for that job.

A Relatable Example

Let's say a small business owner takes out a $150,000 loan to buy new equipment, with a ten-year repayment plan. To protect his family, he buys a ten-year decreasing term policy that starts with a $150,000 death benefit.

If he were to pass away in the second year, the policy would pay out a benefit very close to the initial amount, enough to wipe out the remaining loan and protect the business. But if he passed away in year nine, the payout would be much smaller—but it would still be the exact amount needed to clear that last bit of debt.

That’s the beauty of it. It’s efficient, targeted protection.

Does This Old-School Policy Still Make Sense?

With all the different life insurance policies out there today, you might wonder if something as specific as decreasing term life still has a place. The answer is a definite yes, but only for the right situation. It might feel a bit old-fashioned, but in an economy where every dollar counts, its value is clearer than ever.

Think of it less like a catch-all safety net and more like a specialized tool. It’s designed with a single, laser-focused purpose: to protect your family from a large, specific debt—most often, your mortgage. You’re not paying for extra coverage that becomes unnecessary as the years go by; you're just covering exactly what you owe.

Finding Its Place in Today's Finances

Let's be honest, affordability is a huge factor for most families. This is exactly where decreasing term life shines. It’s a smart, strategic choice for anyone watching their budget because it tackles one of the biggest financial risks—the potential loss of the family home—in the most cost-effective way.

Even with economic ups and downs, the need for targeted protection is always there. The global insurance market insights from marsh.com show that products focused on affordability and specific needs remain popular, especially for shielding families from major debts.

This isn't about getting the biggest possible death benefit; it's about getting the right one. The goal is to make sure your largest single debt is taken care of without you having to overpay on premiums for coverage you won't need in 15 or 20 years.

For families who want to protect their home and legacy with a disciplined, no-nonsense approach, this policy is a practical and valuable solution. It’s a perfect fit for a clear, temporary financial need.

Answering Your Top Questions About Decreasing Term Life Insurance

As you weigh your options, a few practical questions always seem to pop up. Let's walk through the most common ones so you can get a clearer picture of how this type of policy works in the real world.

Can I Own Both a Decreasing and a Level Term Policy?

Absolutely, and for many families, this is the smartest way to go. Think of it like using different tools for different jobs.

You might use a decreasing term policy for one very specific, shrinking debt—your mortgage. At the same time, a separate level term policy can act as a broader financial safety net. That level policy provides a consistent death benefit your family can count on for things like replacing lost income, covering college tuition, or handling final expenses.

This "stacking" strategy lets you cover your biggest debt affordably while ensuring the rest of your family's financial future is on solid ground.

What Happens if I Refinance My Mortgage?

This is a fantastic question and a crucial one to consider. If you refinance, your decreasing term policy can fall out of sync with your home loan.

Let's say you extend your loan term from 15 to 30 years or pull out extra cash. Your old policy was designed to shrink alongside the original loan balance. Your new, larger mortgage balance will now outpace the policy's declining death benefit, potentially leaving a serious coverage gap.

In most cases, if you refinance, you'll need to shop for a new policy that matches the size and schedule of your new loan.

It's important to remember: the death benefit is paid to your beneficiary (like your spouse), not directly to the mortgage lender.

This is a key feature that gives your family control. They receive the funds and can decide how best to use them. While the intention is usually to pay off the house, they have the flexibility to address other urgent financial needs first if necessary.

At America First Financial, we believe in providing clear, straightforward insurance solutions that protect what matters most: your family and your home. Our policies are designed to give you peace of mind, free from political noise. Get a fast, no-hassle quote today and see just how affordable it can be to secure your family's future.

Comments