_edited.png)

How to Set Up an Estate Bank Account A Guide for Executors

- dustinjohnson5

- Aug 29, 2025

- 13 min read

Before you can even think about setting up an estate bank account, there are two crucial pieces of legal paperwork you absolutely must have in hand: your court-issued appointment and a tax ID number for the estate. These aren't just suggestions; they are the non-negotiable foundation for managing the deceased's finances.

Laying the Groundwork for the Estate Account

Being named an executor is a huge responsibility, and those first few steps can feel like navigating a maze. Before you can start consolidating assets or paying off the estate’s debts, you have to prove to the banks that you have the legal authority to act. This isn’t just a bank rule—it’s a legal safeguard to protect the estate’s assets from fraud and ensure they go to the rightful heirs.

Your first stop on this journey is almost always the local probate court. This is where you'll get the official green light to start your duties.

Securing Your Legal Authority

The first document you’ll need is either Letters Testamentary (if the deceased left a will) or Letters of Administration (if there was no will). These court-stamped papers are your golden ticket. They are the official documents that legally certify you as the estate's representative. Without them, no bank will open an account for you. Period.

Pro Tip from the Trenches: When you're at the court clerk's office, ask for multiple certified copies of these letters. I’d suggest getting at least five. You'll need to provide an original certified copy to every financial institution, insurance company, and government agency you deal with. Having extras from the get-go will save you countless headaches and return trips.

Think of these letters as your official credentials—they show everyone you're the person legally empowered to call the shots on the decedent's financial affairs.

To help you get organized, here's a quick rundown of the essential paperwork you'll need to gather before you head to the bank.

Your Initial Document Checklist

Document | What It Proves | Where to Get It |

|---|---|---|

Letters Testamentary or Administration | Your legal authority to act as the estate's representative. | The probate court in the county where the deceased lived. |

Employer Identification Number (EIN) | The estate's unique tax ID, separate from any individual. | The IRS website; the online application is fastest. |

Certified Copy of the Death Certificate | Official proof of the individual's passing. | The county or state vital records office. |

Having these documents ready will make your first meeting with the bank much smoother and show that you're prepared for the role.

Obtaining the Estate's Tax ID

Once the court has officially appointed you, your next immediate task is getting an Employer Identification Number (EIN) from the IRS. For tax purposes, an estate is treated as a separate entity, almost like a small business. It cannot use the deceased's Social Security number, and you certainly can't use your own.

Applying for an EIN is surprisingly simple and can be done online in just a few minutes. This number is mandatory for opening the bank account and is also required for filing the estate's tax returns down the road. It creates a clear, legal separation between the estate's money and your personal funds—a critical part of your fiduciary duty.

To get a full picture of what's expected of you, it's a good idea to look over a comprehensive executor duties checklist to understand all your responsibilities.

According to a 2023 survey, a staggering 85% of executors pointed to delays in getting probate documents or bank cooperation as their biggest hurdles. That’s why it’s so important to move quickly—ideally opening the account within 30 days of your appointment—to prevent any hint of mishandling assets and avoid potential personal liability.

Assembling Your Paperwork for the Bank

Walking into a bank unprepared can turn a simple task into a frustrating, multi-visit headache. When you're setting up an estate bank account, getting it right the first time boils down to one thing: having the exact documents the bank is legally required to see.

Your goal is to build a complete, organized folder that proves, without a shadow of a doubt, that you are the legally appointed representative of the estate. The bank's top priority is compliance, so they simply can't bend the rules on documentation.

The Non-Negotiable Documents

Your folder needs a few core items, and the details are everything. For example, don't just bring a photocopy of the death certificate. You absolutely must have a certified copy—the official one with a raised seal or stamp from the vital records office. This is the only way a bank can legally verify the death.

Your Letters Testamentary or Letters of Administration are just as critical. The bank will look for two things: the official court seal and the date of issuance. Keep in mind that some banks have a policy against accepting documents older than 60 or 90 days, so make sure yours are fresh.

A Real-World Example: I once saw an executor get turned away because their Letters Testamentary were four months old. The bank required a more recently certified copy to ensure their authority hadn't been revoked in the meantime. It was a frustrating delay that was completely avoidable.

Proving the Estate's Identity

The next critical piece of paper is the estate's EIN confirmation letter from the IRS. This is probably the most common point of confusion. You cannot use your personal Social Security number or the decedent's number to open this account. The estate is its own separate legal and tax entity, and the EIN is its tax ID.

Why is the EIN so important? It formally separates the estate's money from your own personal funds, which is a cornerstone of your legal duty as executor.

What does it look like? The confirmation is usually a PDF or a formal letter (Form CP 575) that clearly states the estate's official name and its assigned EIN. Print this out and put it in your folder.

Forgetting this document is an immediate showstopper. The bank simply cannot move forward without it, as it's required for tax reporting on any interest the account earns.

Your Personal Identification

Finally, don't forget about yourself. You'll need your own valid, government-issued photo ID, such as a driver's license or passport. The bank has to verify the identity of the person opening and managing the account—and that's you. Just double-check that it's not expired.

Gathering this paperwork might feel tedious, but it’s the best thing you can do to make the process smooth and quick. It shows the banker you're prepared and professional, which sets a great tone for your entire relationship. Arriving with a complete, organized file makes the task of setting up an estate bank account far less intimidating.

Choosing the Right Banking Partner

Where you decide to bank can make or break your experience as an executor. This isn't just about finding a place to stash the estate's cash; it's about partnering with a financial institution that either gets it or doesn't. Your choice will either make your job a whole lot easier or add layers of frustrating red tape.

The most common move is to just stick with the bank the deceased used. On the surface, it makes perfect sense. They already have the records, they know the person's financial history, and it feels like the path of least resistance. Sometimes, that works out just fine.

But be careful. That convenience can backfire. If you're dealing with a small local bank that sees maybe one estate account a year, you could spend weeks just educating the staff on what you need. On the flip side, a massive national bank might have a dedicated trust department, but their rigid, one-size-fits-all procedures can make you feel like you're just a number in a very long queue.

Should You Stay or Should You Go?

So, do you stick with their bank or find a new one? There’s no single right answer, but here’s how to think it through.

The Case for Sticking Around: The biggest pro is simplicity. Closing the decedent's personal accounts and rolling the money directly into a new estate account at the same institution can be incredibly smooth.

When It Gets Complicated: If the deceased had loans, lines of credit, or other complex financial ties to that bank, things can get messy. You don't want the estate's assets tangled up with outstanding debts in a way that complicates settlement.

The "Clean Slate" Approach: Starting fresh with a new bank lets you call the shots. You can pick an institution known for its expertise in estate accounts, with a fee structure that makes sense and customer service that actually serves you.

The idea of a separate bank account just for an estate isn't new, but how we manage them has changed drastically. As estates have become more digitally complex, choosing a bank with solid legal and tech support is more critical than ever.

Banking regulations have also gotten much stricter. For instance, since 2000, the Patriot Act has required US banks to perform much deeper checks, meaning they'll need to verify your identity as the executor and the source of the estate's funds. You can find more insights on how global financial trends impact estate management on pwc.com.

Key Questions to Ask Any Potential Bank

Before you walk in with a death certificate, do some homework. Call or visit a few banks and interview them. Remember, you're hiring them to help you manage this process correctly.

Here’s what I always ask:

Do you have a dedicated estate specialist or a trust department? This is the most important question. You need to speak with someone who knows what "Letters Testamentary" are without you having to explain it.

Can you give me a checklist of every single document you require? Get this upfront. Nothing is more frustrating than making multiple trips to the bank because someone forgot to mention one more form.

What are all the fees for an estate account? Dig into the details. Ask about monthly maintenance fees, check printing costs, and especially wire transfer fees, as you'll likely be making distributions.

Realistically, how long does it take to open an estate account here? Their answer will tell you a lot about their internal processes and efficiency.

Finding a banker who gives you clear, confident answers is a huge green flag. It’s a sign that they’ve done this before and won’t be the source of a bottleneck later on. A little bit of due diligence now will save you countless headaches down the road.

Meeting the Banker and Opening the Account

Alright, you've gathered all your documents and have everything neatly organized. Now it’s time for the final piece of the puzzle: heading to the bank. This is where all that prep work really pays off. Your goal here is simple: walk out with a fully operational, correctly named estate account.

The single most important detail in this entire meeting is getting the account title perfect. It has to be worded in a very specific legal way to show it's a fiduciary account. This isn't just a bank being picky; it's a critical legal and tax requirement.

Nailing the Account Title

Let's be crystal clear: this account can't be in your name, and it can't be in the deceased's name either. It must be titled to show it belongs to the estate, with you acting as the manager. The standard, and correct, format is:

"Estate of [Decedent's Full Name], [Your Full Name], Executor"

So, if you’re John Smith and you’re the executor for Jane Doe’s estate, the account title must read: "Estate of Jane Doe, John Smith, Executor." Getting this exact phrasing is non-negotiable. It creates a legal firewall between the estate’s money and your personal funds, which protects you from liability and keeps the tax reporting squeaky clean.

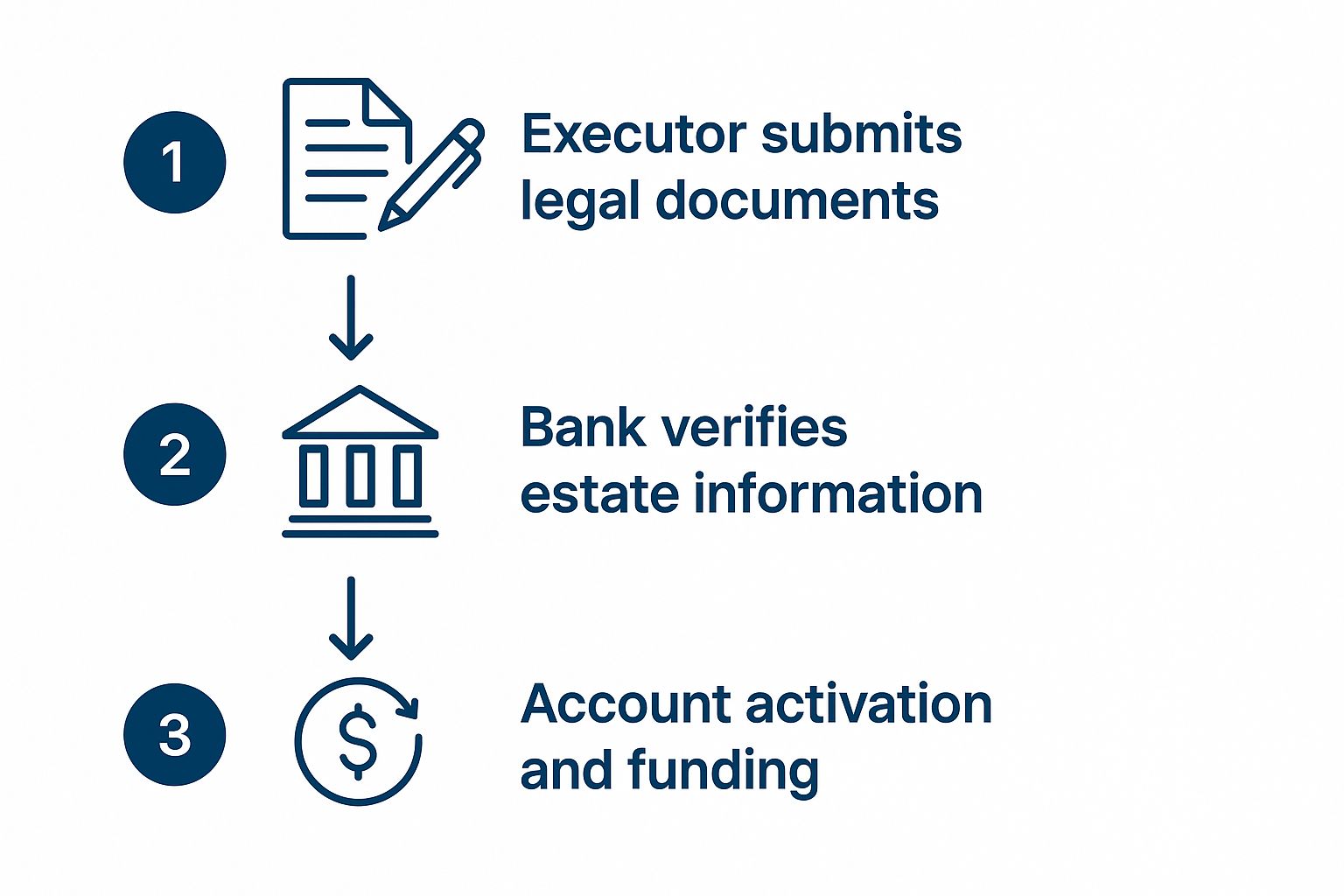

This quick visual breaks down the core steps you'll take at the bank to get things up and running.

As you can see, it's a straightforward sequence. The bank verifies your legal authority based on the documents you provide, and then the account is ready to be funded and used.

Making the First Deposit

With the account officially created, the next step is to put some money in it. The initial funds will almost always come from the deceased's personal bank accounts. You'll use your Letters Testamentary to authorize the bank to close those accounts and roll the balances directly into the new estate account.

But what happens when checks made out to the deceased start showing up in the mail? It’s a common scenario.

Once the estate account is open, you can deposit checks made out to the decedent directly into it. The bank, having seen the death certificate and your legal appointment, will endorse them on behalf of the estate. This is the only proper and legal way to handle such payments.

Setting Up the Right Account Features

Before you shake hands with the banker and leave, make sure the account is set up with the tools you'll actually need. Don't let them open a simple savings account for you. A checking account is what you want—it provides the flexibility you need to pay the estate’s debts and, eventually, distribute assets to the heirs.

Make sure you walk away with these features enabled:

Checks: You’ll need to order a set of checks printed with the estate's official name. These are what you'll use to pay creditors, legal fees, and any other expenses that pop up.

Debit Card: While you should be cautious, a debit card can be handy for small, direct purchases related to the estate, like buying cleaning supplies for the deceased's home.

Online Access: This is absolutely essential. Online banking gives you a clear, real-time log of every transaction. This digital paper trail is invaluable for your accounting duties and for keeping the beneficiaries informed.

Leaving the bank with a functional, correctly titled estate account is a huge step forward. You now have the official financial tool you need to manage the estate responsibly and with total transparency.

Managing the Estate Account Responsibly

Alright, the estate bank account is officially open. Now, your job pivots from setup to careful management. As the executor, you've stepped into a fiduciary role. That’s a legal way of saying you have a sworn duty to act solely in the best interest of the estate and its beneficiaries.

This isn’t about just holding the money; it's about stewardship. Your mission is to manage this account with absolute precision and transparency. Every single transaction, no matter how small, needs to be documented. Think of it this way: your records are your best defense against any potential questions or legal challenges down the road. You’re building a clear, unshakeable financial story of the estate.

The Golden Rule of Estate Management

If you remember only one thing, make it this: never commingle funds. Your personal money and the estate's money must live in completely separate worlds.

Even a small mistake, like accidentally paying your own utility bill from the estate account or depositing a check meant for the estate into your personal account, can spiral into a legal and tax mess. It muddies the waters and can raise serious questions about your impartiality. Keeping that hard line between your finances and the estate's protects you and gives the court and beneficiaries a crystal-clear audit trail.

Executor's Duty: Your responsibility is to act as a guardian of the estate's assets. Meticulous record-keeping and a strict separation of funds are not just best practices—they are the core of your legal obligation and provide peace of mind to everyone involved.

Remember, this isn’t a short-term gig. The probate process, during which this account will be your primary tool, often lasts between 14 to 18 months. Throughout that time, your diligent accounting will be crucial for beneficiaries and tax authorities. For a broader perspective, you can find more insights on global financial account trends on worldbank.org.

Day-to-Day Account Management in Practice

So, what does responsible management look like on a practical level? It's about using the account exactly as intended: to gather the estate’s assets, pay its bills, and get everything in order for the final distribution to the heirs.

Here’s what you’ll be doing with the estate account:

Consolidating Assets: This account becomes the central hub for all money coming into the estate. You'll deposit everything here—from life insurance payouts and final paychecks to the funds from selling the deceased’s car or house.

Paying Legitimate Debts: The deceased's final bills must be paid from the estate’s funds. Use the estate account to handle credit card balances, outstanding medical bills, and funeral expenses. Always pay with a check or the account's debit card, never cash. You need that paper trail.

Covering Administrative Costs: Any expenses you incur while doing your job as executor are paid from this account. This includes things like court filing fees, paying for an attorney's advice, or hiring someone to maintain the deceased’s property.

Stick to these practices, and every financial move you make will be easy to justify. This level of detail not only satisfies your legal obligations but also fosters trust with the beneficiaries, which can make a difficult process run much more smoothly for everyone.

Common Questions About Estate Bank Accounts

Even with the best plan, you're going to hit a few snags or have questions pop up when setting up an estate bank account. It just comes with the territory. Think of this as your go-to guide for those "what do I do now?" moments that inevitably arise.

Getting these little details right is just as important as the big steps. A small mistake can easily lead to delays, so let's clear up some of the most common issues executors face.

What If I Need to Pay an Expense Before the Account Is Open?

This is probably one of the most frequent questions I hear. The probate process isn't exactly fast, but bills for the funeral home or the mortgage on the deceased's house simply can't wait. It’s a classic catch-22.

So, what do you do? The practical solution is to pay for these legitimate estate expenses out of your own pocket for the time being.

But you have to be incredibly careful about how you do it.

Keep Meticulous Records: This is non-negotiable. Save every single receipt and invoice. I recommend scanning them or taking a photo right away so you have a digital backup.

Create a Reimbursement Log: A simple spreadsheet will do the trick. Log every expense: date, amount, vendor, and what it was for. This creates a crystal-clear paper trail.

Reimburse Yourself Properly: Once the estate account is open and has funds, you can write a check from that account to yourself for the exact amount you're owed. This isn't just "getting your money back"—it's a formal, documented transaction that keeps everything above board for the court and beneficiaries.

This approach keeps you from illegally commingling funds while still taking care of the estate's immediate obligations.

What Do I Do with Checks Made Out to the Deceased?

Sooner or later, a check is going to show up in the mail addressed to the person who has passed away. It could be anything—a tax refund, a final paycheck, a dividend from some old stock. Whatever you do, don't try to cash it or deposit it into your own account. Banks will reject it, and it could raise serious red flags.

The only proper home for these funds is the estate bank account. Once the account is set up in the name of the estate (like "Estate of Jane Doe, John Smith, Executor"), you can endorse the check and deposit it. Your Letters Testamentary or Letters of Administration are your proof to the bank that you have the legal right to handle that check.

Key Takeaway: The estate account is the financial heart of the estate. Every dollar that belonged to the deceased or is owed to them must flow through this single account. This creates the clean, transparent record you'll need later.

Do I Ever Need More Than One Estate Account?

For the vast majority of estates, a single checking account is all you'll ever need. Honestly, it's the best way to go. It dramatically simplifies your bookkeeping and keeps all the financial activity—collecting assets, paying bills, distributing inheritances—in one place.

That said, there are some rare and complex situations where a second account might make sense. For instance, if the estate includes an active business or a portfolio of rental properties, having a separate account just for those operations can make tracking that specific income and its expenses much easier. But for 99% of executors, one well-managed account is the standard and the smartest choice.

At America First Financial, we believe in protecting your family's future with clear, dependable solutions rooted in traditional values. If you're looking for insurance coverage that aligns with your principles, get a no-hassle quote today. https://www.americafirstfinancial.org

Comments