_edited.png)

What Is a Health Savings Account Explained

- dustinjohnson5

- Oct 18, 2025

- 12 min read

A Health Savings Account, or HSA, is a special savings account that lets you put money aside for healthcare costs while getting some incredible tax breaks. The simplest way to think about it is as your own personal savings account, but one that’s only for medical expenses.

The real magic is its triple-tax advantage: your contributions can be tax-deductible, the money grows tax-free, and you can pull it out tax-free for qualified medical needs.

Your Guide to Health Savings Accounts

Imagine a financial tool that blended the best parts of a savings account, a 401(k), and a dedicated medical fund into one powerful package. That’s an HSA in a nutshell. It’s your personal health fund, designed to give you a tax-smart way to prepare for both routine and unexpected medical bills.

There's one catch, though. An HSA doesn't work on its own; it has to be paired with a specific type of insurance called a High-Deductible Health Plan (HDHP). This partnership is what makes the whole system click. The HDHP is there to cover you for major health events, while your HSA helps you pay for the smaller, day-to-day costs that come up before you meet your deductible.

To give you a quick overview, here are the core features of an HSA.

Health Savings Account (HSA) at a Glance

Feature | Description |

|---|---|

Eligibility | Must be enrolled in a High-Deductible Health Plan (HDHP). |

Tax Benefit | Triple-tax advantaged: tax-deductible contributions, tax-free growth, tax-free withdrawals. |

Ownership | You own the account and the funds are yours, even if you change jobs or retire. |

Rollover | Funds never expire. Unused money rolls over year after year. |

Investment | You can often invest your HSA funds in stocks or mutual funds for long-term growth. |

This table covers the basics, but let's dig a little deeper into what makes these accounts so powerful for families.

Core Features of an HSA

The real strength of an HSA comes from a few key features that make it completely different from a regular savings or checking account. Once you get these, you'll see why it’s such a smart tool for managing family finances.

You Own the Account: The money in your HSA is yours. Period. It isn’t tied to your job, so if you switch employers or even retire, the account and every penny in it go right along with you.

Funds Roll Over: There's no "use-it-or-lose-it" panic at the end of the year. Any money you don't spend automatically rolls over to the next year, letting you build a serious health fund over time.

Investment Potential: Many HSAs give you the option to invest your money in mutual funds or stocks, just like you would with a retirement account. This means your balance has the potential to grow much faster than it would sitting in a standard savings account.

An HSA offers a unique combination of tax savings and healthcare planning. It empowers you to take control of your medical expenses while building a financial safety net for the future.

This structure gives you a level of flexibility and long-term benefit that goes way beyond just paying for a trip to the doctor. It's a strategic way to make your healthcare dollars work a lot harder for you.

How a Health Savings Account Actually Works

To really get what a Health Savings Account is all about, you have to see it as part of a team. An HSA doesn't work on its own; it has a required partner: a specific type of health insurance called a High-Deductible Health Plan (HDHP).

Think of it this way: your HDHP is the safety net, protecting you from huge, unexpected medical bills. The HSA, on the other hand, is your day-to-day tool for handling all the routine healthcare costs that pop up.

First things first, you can only open and contribute to an HSA if you’re enrolled in a qualified HDHP. That’s the non-negotiable rule. The good news is these plans often come with lower monthly premiums than traditional insurance, which frees up money you can put straight into your HSA.

We’re seeing a big shift in how people handle their health expenses. The number of private industry workers with an HDHP jumped from 38% in 2015 to 50% in 2024, making HSAs more common than ever. If you're curious, you can discover more insights about how these plans have grown and what that means for families.

The Mechanics of Funding Your HSA

Once you're set up with an eligible health plan, funding and using your HSA is surprisingly simple. It feels a lot like a regular savings account, just one with some incredible tax benefits and a specific purpose.

Money can get into the account in a few different ways:

Your Contributions: You can transfer money from your bank account or, even easier, set up automatic payroll deductions.

Employer Contributions: Many companies will kick in some money to their employees' HSAs as a perk. It's a great way to get a head start on your savings.

Family Contributions: Anyone—a parent, grandparent, you name it—can contribute to your account, as long as the total stays within the annual limit.

All these contributions just pool together in your account, waiting for you when you need them.

An HSA acts like a '401(k) for healthcare.' It's not just a spending account for today; it’s a powerful savings vehicle that allows your money to grow tax-free for future medical needs.

This is what makes an HSA so special. It serves two purposes—letting you spend on immediate needs while also helping you save for the long haul. It's a fantastic tool for any family looking to get a handle on their financial and physical health.

Contribution Limits and Using Your Funds

Every year, the IRS sets limits on how much you can put into your HSA. They adjust these numbers from time to time to keep up with inflation and the rising costs of healthcare.

For 2024, the contribution limits are:

$4,150 if you have self-only coverage.

$8,300 if you have family coverage.

There's also a little bonus for those nearing retirement. If you're 55 or older, you can add an extra $1,000 each year as a "catch-up" contribution.

When you actually need to pay for something, using your HSA is a breeze. Most HSA providers give you a debit card linked to your account. You can swipe it at the doctor's office, pharmacy, or dentist for any qualified medical expense. Or, you can pay for something out-of-pocket and just reimburse yourself from the HSA later. It gives you a lot of flexibility.

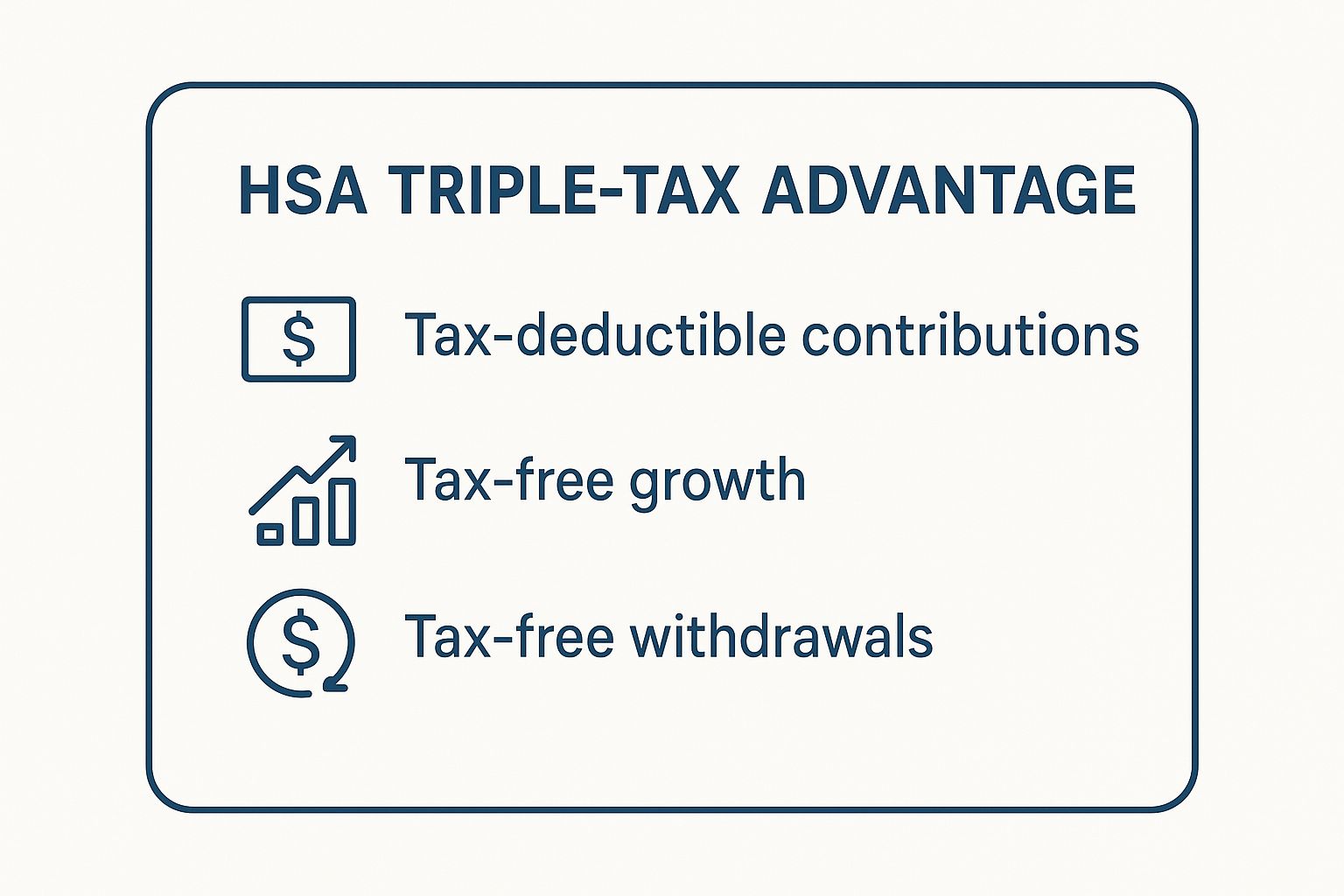

The HSA's Secret Weapon: The Triple-Tax Advantage

So, what makes a Health Savings Account so different from any other savings plan out there? It all comes down to one incredible feature: the triple-tax advantage. This isn't just a minor benefit; it’s the powerful engine that transforms an HSA from a simple healthcare fund into one of the most effective financial tools available for your family.

This advantage works its magic at three different points: when you put money in, while it grows, and when you take it out. Once you see how these three benefits stack up, you'll understand why the HSA is in a class of its own. Let's break it down.

1. Your Contributions are Tax-Deductible

The first benefit hits right away. Every single dollar you contribute to your HSA is 100% tax-deductible for that year. This directly lowers your taxable income, which means you’ll owe less to the IRS when tax season rolls around.

Think of it this way: if you’re in the 22% federal tax bracket and you put $4,000 into your HSA, you could instantly shave $880 off your federal tax bill. That’s a direct and immediate savings that puts money right back into your family’s budget.

The infographic below really helps visualize how all three of these tax breaks work together.

As you can see, every stage—from deposit to growth to withdrawal—is completely shielded from taxes. You'd be hard-pressed to find another account that can do that.

2. Your Money Grows Completely Tax-Free

The second advantage is where the HSA really starts to shine over the long haul. In a normal savings or investment account, you’d owe taxes on any interest or gains your money earns. Not with an HSA. The money in your account grows completely tax-free.

Many HSAs even let you invest your balance in mutual funds, stocks, and other assets, just like a 401(k). All the earnings from those investments—dividends, interest, capital gains—are yours to keep, untouched by taxes. This allows your balance to compound much faster over the years, turning your savings into a serious nest egg.

An HSA's ability to grow without being taxed on its earnings is what elevates it from a healthcare spending account to a legitimate retirement planning tool.

It’s this tax-free growth that truly puts your money to work, building a fund you can rely on for future medical needs.

3. Withdrawals for Medical Costs are Also Tax-Free

And finally, the third piece of the puzzle. When it’s time to use your funds, you can pull money out for any qualified medical expense without paying a dime in taxes.

This covers a huge range of healthcare costs your family might face. We're talking about everything from the routine to the unexpected:

Doctor’s visits and specialist co-pays

Prescription drugs

Dental cleanings, fillings, and braces

Vision exams, glasses, and contacts

Hospital stays and surgical procedures

From the moment you deposit a dollar to the moment you spend it on healthcare, it never gets taxed. This end-to-end tax protection is precisely what makes the HSA such a uniquely powerful way to manage your family's health expenses, both today and for decades to come.

Comparing an HSA vs FSA

When people first learn about HSAs, their next question is almost always about the Flexible Spending Account, or FSA. It's a natural comparison. Both accounts let you set aside pre-tax money for medical expenses, but that's where the similarities end.

Think of them as two different tools for two very different jobs. Understanding how they work is crucial for picking the right one for your family’s financial goals. The biggest differences boil down to who owns the money, whether it expires, and how much control you have over the long haul.

At its core, an HSA is a personal savings account for healthcare that you own outright—forever. An FSA, on the other hand, is an account owned by your employer, which comes with some pretty strict rules on how and when you can use the cash.

Who Actually Owns the Money?

This is the first, and arguably most important, distinction. The money in your Health Savings Account is yours. Full stop. It doesn’t matter if you switch jobs, get a different health plan, or retire. That account and every penny inside it belongs to you and goes wherever you go. That kind of portability gives you incredible control and peace of mind.

FSAs are a different story. They are tied directly to your employer. If you leave your job, you typically have to say goodbye to any money left in the account. This makes an FSA a less flexible choice for anyone thinking about the future.

The core principle to remember is simple: You own your HSA, but your employer owns your FSA. This single distinction influences nearly every other aspect of how these accounts function.

This fundamental difference in ownership leads us straight to the next critical feature: what happens to your money at the end of the year.

The Famous “Use-It-or-Lose-It” Rule

Here’s the difference everyone talks about. An HSA has no expiration date. Ever. Any money you don't spend this year simply rolls over to the next, and the next, and the next. This allows you to build a substantial healthcare fund over time, which can even be invested.

FSAs are notorious for their “use-it-or-lose-it” rule. At the end of the plan year, you generally forfeit any unspent funds. Some employers might offer a small rollover (up to $640 for 2024) or a short grace period to spend the rest, but the pressure to drain the account is always there.

HSA vs FSA Key Differences

To really see how these two accounts stack up, it helps to put them side-by-side. The table below breaks down the most important features to consider.

Feature | Health Savings Account (HSA) | Flexible Spending Account (FSA) |

|---|---|---|

Account Ownership | You own the account and it's fully portable. | Your employer owns the account. |

Fund Rollover | Funds always roll over year after year. | Funds are generally "use-it-or-lose-it." |

Eligibility | Must be enrolled in a High-Deductible Health Plan (HDHP). | Available with most employer-sponsored health plans. |

Investment Option | Yes, you can invest funds for tax-free growth. | No, funds cannot be invested. |

Contribution Source | You, your employer, or anyone can contribute. | You and your employer can contribute. |

Ultimately, the choice comes down to your goals. An HSA offers incredible freedom and acts as a powerful long-term savings and investment vehicle. An FSA, while still a great tool for handling predictable annual medical bills, is a much more restrictive, short-term solution.

Using Your HSA for Long-Term Growth

Most people see their HSA as just another way to pay for doctor's visits and prescriptions. But that’s only scratching the surface. The real power of an HSA is unlocked when you start treating it less like a checking account for medical bills and more like a retirement account for your health.

The big shift is mental: from short-term spending to long-term investing. Many HSA providers let you invest your balance in mutual funds, ETFs, and stocks—the same kind of options you’d find in a 401(k). And because of that incredible triple-tax advantage, every single dollar your investments earn grows completely tax-free. Over decades, that compounding effect can be massive.

The Power of Investing Your HSA Funds

Let's run some simple numbers. Say you contribute $4,000 to your HSA every year for 25 years. If you just let it sit in cash, you’ll have $100,000. Not bad.

But what if you invested it? Assuming a pretty average 7% annual return, that same $4,000 per year could balloon to over $250,000. And every penny of that growth is yours to use, tax-free, for qualified medical expenses.

This is why you'll often hear financial pros call the HSA a "stealth IRA." It's a retirement powerhouse hiding in plain sight. Shockingly, though, most people aren't taking advantage of it. Research shows that only about 15% of HSA owners actually invest their funds. That's a huge missed opportunity for families to build a tax-free nest egg.

When you invest your HSA, you transform it from a simple spending tool into a core part of your financial future. It becomes a dedicated, tax-advantaged fund ready and waiting for whatever healthcare costs come your way in retirement.

The most effective way to grow your HSA is to contribute the maximum allowed each year and, if possible, pay for current medical expenses with other funds, leaving your HSA balance to grow untouched.

This strategy definitely takes some discipline, but the payoff down the road is enormous. When you treat your HSA as an investment-first account, you let the magic of compounding do the heavy lifting for you.

Your HSA as a Retirement Account

Once you hit retirement age, the HSA gets even better. After you turn 65, it essentially moonlights as a traditional retirement account, giving you penalty-free access to your money for any reason at all.

Here’s the breakdown:

For Qualified Medical Expenses: Withdrawals are still 100% tax-free, just like always. This is perfect for covering Medicare premiums, long-term care insurance, or any out-of-pocket health costs.

For Any Other Reason: Need money for a vacation, home repairs, or just living expenses? No problem. You can pull money out for non-medical reasons. You'll just pay ordinary income tax on the withdrawal, exactly like you would with a 401(k) or traditional IRA. The key difference is that the steep 20% penalty for non-qualified withdrawals completely disappears.

This dual-purpose nature makes the HSA one of the most flexible financial tools out there. It’s a tax-free war chest for healthcare costs, but it also serves as a fantastic backup retirement fund. By truly understanding and using its investment features, you can set your family up for financial security, no matter what the future holds.

Common HSA Questions Answered

Even after you get the hang of what a Health Savings Account is, the real questions start to pop up once you try to use it in your day-to-day life. This is where theory meets reality. Let’s walk through some of the most common situations you’ll likely run into.

One of the first questions people ask is about changing jobs. What happens to my HSA if I leave my company or switch to a different health plan? The good news is, the answer is simple: nothing happens to your account. You own your HSA outright, so it's completely portable. That account and every dollar in it is yours to keep, no matter where you work.

The only thing that changes is your ability to add more money. You can only contribute to an HSA during the months you're covered by a qualified High-Deductible Health Plan (HDHP). If you move to a more traditional PPO or HMO plan, you can’t put new money in, but you can absolutely still spend your existing HSA balance on any qualified medical expense that comes up.

Who Can You Use Your HSA For?

People also wonder if their HSA is just for them or if it can cover family members. The answer here is a definite yes. You can use your HSA to pay for the qualified medical expenses of:

Yourself (the account owner)

Your Spouse, even if they aren't on your HDHP

Your Dependents, like your children or any other relatives you claim on your taxes

This flexibility is a huge advantage, turning your HSA into a powerful tool for managing healthcare costs for your entire family from one single, tax-advantaged account.

Think of your HSA less as a personal health fund and more as a family health fund. The money is there for the qualified medical needs of your spouse and dependents, giving you one central, tax-smart way to manage everyone's care.

This broad usability means your savings can go wherever they're needed most to support the well-being of your loved ones.

What Expenses Are Actually Covered?

The phrase "qualified medical expenses" covers a much wider territory than most people think. It goes way beyond just doctor visits and prescriptions. For instance, it's helpful to understand what preventive dental services insurance typically covers, as these are almost always eligible HSA expenses, too.

Here’s a quick look at just some of the things you can pay for tax-free with your HSA:

Medical Services: Doctor visits, hospital stays, co-pays, and lab work.

Dental Care: Everything from cleanings and fillings to braces and even dentures.

Vision Care: Eye exams, prescription glasses, contacts, and LASIK surgery.

Prescriptions: Any medication prescribed by a doctor.

Mental Health: Therapy, counseling, and psychiatric appointments.

Alternative Treatments: Chiropractic adjustments and acupuncture often qualify.

This wide range of coverage gives you the confidence to use your account for nearly any health-related need that arises for you or your family.

At America First Financial, we believe in providing clear, straightforward solutions that help you protect your family’s financial future. Discover how our health care plans can work with your HSA to provide security and peace of mind. Get a free, no-hassle quote today at https://www.americafirstfinancial.org.

Comments